What’s Your Cash Flow: Interest Rate by Credit Score

Categories: Blog Posts

Lenders decide your interest rate by credit score. Here’s how it shakes out…

Leverage is the lifeblood of investing… Using other people’s money (loans) to create income and wealth for you and your family.

The largest source of funding is both small and large lending institutions. One of the top (if not the top) determining factors for lenders getting you the best funding possible… is your credit score.

Let’s look behind the scenes and see how these lenders use credit scores to determine your rate.

How Lenders Decide Interest Rate by Credit Score

Full disclosure: sometimes your rate gets jacked up just because you’re working with a greedy loan officer.

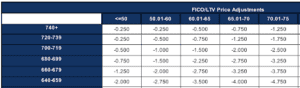

However, once you’ve found a lender you trust, you can be assured they’re using an internal system that looks something like this:

These credit boxes are what the lender uses to determine the cost of a good vs not so good credit score. (If your score is too low, you more than likely will just not get a loan).

The above example is what we would see from a typical DSCR lender. A conventional lender’s would look very similar.

The negative price adjustments are not a direct change to a rate but they are added to the cost to calculate the rate. In layman’s terms: the higher the cost, the higher the rate.

From the highest score to the lowest, you would expect to see around a 1.5% increase in interest rate. So, if the best rate was 7% at a 740+ credit score, then you may expect a rate of 8.5% with a 640 score.

Example: How Interest Rates and Credit Score Changes Your Cash Flow

As an example, let’s say we need a $300,000 loan for either a purchase or refinance. The cost of our funding, depending on interest rate, would be:

- At 7%, the monthly payment would be $1,996

- At 8.5%, the monthly payment would be $2,306

How does that look in credit terms? A 640 score would cost you the $2,306. On the other hand, a 740 score would cost you $300 less, at $1,996.

This is a $300 difference per month in your cash flow. Aka: a bad credit score could cost you $3,600 per year in cash flow!

An investor with a great credit score and 10 properties would be paying $1 million less over the life of their loans than an investor with the same amount of properties and bad credit.

Help with Your Cash Flow

This is why investing is easier for some people and harder for others:

Cash flow is king.

Credit will control that cash flow.

Want to find out how to get your credit score up and your rates down?

To get our report on the best rates, reach out to us at Info@TheCashFlowCompany.com. You can also get more info on real estate investing on our YouTube channel.

")

")