Using two BRRRR loans creates a rental property for $0. Here’s how.

Are you ready to take your real estate investing to the next level with the BRRRR strategy? You’ll want to get a firm grasp on the two key loans that make it all possible: the buy loan and the refinance loan.

In this blog post, we’ll dive into the nitty-gritty of BRRRR loans and show you how to use them to build wealth through real estate.

Why Use 2 BRRRR Loans?

In the BRRRR method, you need two loans – one to buy, and one to refinance. One short-term, and one long-term. One investor-friendly loan, and one conventional.

This two-loan strategy allows you to unlock the equity hidden in a BRRRR-style under-market property.

But why do you need the first loan? Why can’t you just buy with a conventional loan rather than something like hard money?

Let’s look at an example of what happens if you purchase investment properties using traditional versus investor-friendly BRRRR loans.

Traditional Loans vs Investor-Friendly BRRRR Loans

Here are the specs on our example property:

- After-repair value (ARV): $400,000

The appraised value of this house should be $400k once we’re at the refinance stage.

We’re going to buy this property for $300k.

In most actual BRRRR situations, we’d need to consider rehab costs in the equation. For the sake of our example, though, let’s say this house is rent-ready at $300k.

The spirit of BRRRR is to buy houses under-market – for less than they’re actually worth. This example house costs $300,000, but it’s worth $100k more, at $400,000.

Using Traditional BRRRR Loans for Purchase

With a traditional loan, like a 30-year fixed mortgage, Fannie or Freddie, or other conventional, the lender has to abide by underwriting rules. When it comes to using appraised value or purchase price for the LTV, the rules say the lender has to use the lower of the two numbers.

So if you purchase for $300k, even if the home is worth $400k, they can only loan you for the purchase. In addition to that, they’ll also require 20% commitment.

What does this chalk up to for your wallet?

- The lender will give you a loan-to-value of 80% of $300,000. So the actual loan you get is $240,000.

- You’ll need to bring in $60,000 for the purchase of the property.

Buying a BRRRR with a traditional loan means a smaller loan and a big down payment.

And that’s just not what BRRRR is meant for. The BRRRR strategy should be a zero-down, high-leverage real estate method.

So how do you get there?

Using Investor BRRRR Loans

Let’s check out our example house if we used an investor-friendly loan for the purchase.

Using an investor real estate loan, like hard money, allows you to profit using two BRRRR loans. This first loan is to buy at the lower listed price, the other is to refinance with the full appraised value of the home.

Remember that the traditional loan went wrong when the underwriting guidelines forced us into a lower loan amount. But when you buy with a hard money loan… that underwriting suddenly opens up.

During a purchase, investor-friendly loans look at the value of the home, the ARV. They base the loan amount on this number, which does two things:

- Gives you more money to work with on a rehab.

- Requires less (or often no) money down.

Investor-friendly loans often offer 75% or higher LTV for the ARV.

In our example, this means your investor-friendly loan will cover $300,000 (which is 75% of the $400k). This gives you enough to purchase the property with no money down required.

Now, what happens with that $100,000 gap between what we bought the house for and what it’s worth? Let’s look at how to capture that equity.

The Refinance Stage of the BRRRR Process

Buying a BRRRR with a traditional loan is limiting. Refinancing a BRRRR with a traditional loan is freeing. Let’s see how these BRRRR loans shake out once we get to the refinance stage.

Firstly, there are two types of refinances.

A cash-out refinance turns the equity in the house into cash. A rate-and-term refinance is more like trading your old loan for a new one. Cash-out loans are usually 5-10% less than a rate-and-term.

Refinancing Out of a Traditional Loan

Now, let’s go back to our example and compare the refinances when we used traditional vs investor-friendly BRRRR loans to buy the property.

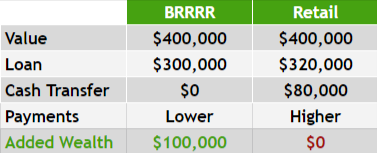

Remember that our BRRRR property is worth $400,000. We bought it with the traditional loan for $300,000. We have a loan for $240,000.

In this case, we have to do a cash-out. We’re already out $60,000 from the down payment, so we want the most we possibly can get back in our pockets.

For a cash-out refinance, you’ll likely be limited to a 70% LTV on the value of the home which is, in this case, $400,000. This means we’ll get a new loan for $280,000.

That still doesn’t cover the $300,000 total we paid for the house, so we’re still losing $20,000 on the deal.

Refinancing Out of a Hard Money Loan

But the point of BRRRR loans is that you can complete the project with zero money down.

So now let’s look at how the investor-friendly loan set us up for the refinance.

With this hard money loan, we bought the house for $300,000 and now have a loan for $300,000. So far, we’ve put $0 of our own money into the property.

We’ll be able to use a rate-and-term refinance. We don’t need to get cash for ourselves – we just need to pay off our first lender.

Let’s say you’re still able to get a 75% LTV on the value of $400,000. Our refinance comes out to exactly $300,000, perfectly covering our loan.

This is how investor-friendly BRRRR loans let you invest in real estate with zero down!

You Can Do BRRRR

Knowledge, planning, and understanding makes all the difference with a BRRRR. We see many beginner investors make simple mistakes with their two BRRRR loans. Too many people put tens of thousands of dollars into a property that should have been $0.

- Don’t use a traditional loan until you own the property and are ready to refinance.

- Use an investor-friendly lender upfront for the purchase. This will always maximize your leverage and shrink your money down.

- Do an investor-friendly rate-and-term refinance.

Have questions on the numbers of your BRRRR project? Need an investor-friendly loan? We’re happy to help. Send us an email at Info@TheCashFlowCompany.com.