Busting Myths: How You CAN Afford Hard Money

It’s time to start busting myths about hard money, and discover how you CAN afford hard money.

Today, we’re going to bust one of the most common misconceptions about this investor-friendly lending option:

“Hard money is too expensive!”

False!

When you get a hard money loan, it doesn’t mean you have to automatically pay 12% interest or more.

In fact, if you take these 3 steps, the cost of your hard money loan will be drastically reduced:

Prove you have experience.

If you show a hard money lender you’ve completed real estate deals successfully, then they’ll feel more confident in giving you money. And confidence means better rates.

How can you show your experience? The best way is to present a real estate portfolio with before and after pictures, budgets, and profits earned.

Be willing to put money down at closing.

If you have skin in the game, then a lender will likely be more willing to lower the cost of your loan. Why? Because it reduces their risk.

But how much money should you try to put down at closing? Ideally, 10% or more. But even as much as 5% will help lower your loan’s cost.

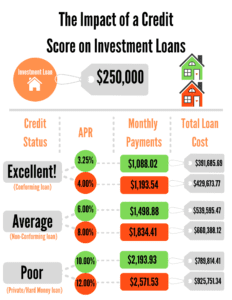

Maintain a good credit score.

Your credit score matters when it comes to loans. The better your score, the better your rates.

If your credit score is on the low side (below 670), then you can find simple ways to boost it. Here are 3 tips to get you started:

- Stop using your credit card and start paying it off. Simple, but effective. And when you hit a $0 balance, do NOT close the account. Closing an account that’s in good standing is anti-productive in keeping your score healthy. You want to show you have good credit history. So if you close your accounts, then your history won’t exist.

- Keep your card balance low. Like, under 30% of its maximum. So, if your card has a maximum credit line of $1,000, then don’t let your balance rise above $300.

- Pay your credit card bill on time. Again, simple, but effective. If you make your payments on time for the next 12 months, your score WILL rise.

Hard money doesn’t have to eat up all of your profits. We assure you that if you take these 3 steps, you can greatly reduce your costs and actually boost your profits considerably.

Stay tuned for our next video where we discuss the myth of getting trapped in a hard money loan. Spoiler alert, another pitfall that’s easily avoidable if you take a few simple steps.

Ready to chat about your hard money and other lending options? Great! Our team is here to help.

What is hard money? Learn more on our YouTube channel!

Happy investing!