It’s “the easy loan.” But are DSCR loans good for your investments?

DSCR loans are becoming one of the most popular investor tools out there.

But why are they so well-loved? Let’s go over 5 reasons investors like DSCR loans.

Are DSCR Loans Good?

Firstly, let’s go over what a DSCR loan is.

DSCR stands for “debt service coverage ratio.” They’re a loan for rental properties that are based on the debt ratio of rent income to the property’s expenses.

These loans can be flexible and hassle-free. This makes them the go-to choice for investors financing a rental property or turning a fix-and-flip project into a rental at the last minute in bad markets.

But are DSCR loans really as good as they seem? Let’s take a closer look at 5 reasons why DSCR loans are a solid choice for investors.

#1: You can start investing now.

DSCR loans are great for new investors. Traditional loans often require you have two years of real estate investing experience.

Because there are no experience requirements, a DSCR loan is a great opportunity to get into your first investment rental property. Don’t wait to apply for your first DSCR loan.

#2: No income requirements.

With a DSCR loan, you don’t have to have a W2 job, or show any tax returns or other income documentation.

This means DSCR loans are good for minimizing your tax liability. You can write everything off, pay the IRS as little as you want, and still get a great loan.

#3: Less paperwork.

The investor’s dream: less paperwork. Applications and approvals are simple with DSCR loans. There are no income requirements, employment verification, or any other intensive qualifications.

Not only is it less hassle to skip some paperwork – it also means the entire loan process is much faster.

#4: DSCR works for short-term rentals too.

DSCR loans don’t just work for traditional rentals, but they work for all real estate investment properties. DSCR loans are flexible and work with a variety of rental options. This includes VRBO, Airbnb, or renting out a traditional long-term property.

There are a few things to take into consideration with short-term rentals and DSCR. But it’s still a simple and often profitable loan for these types of properties.

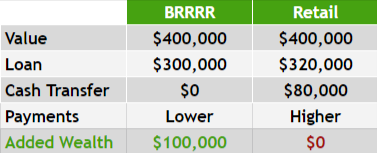

#5: Great for BRRRRs.

Many investors wonder – are DSCR loans good for BRRRR-style properties? The answer is yes.

DSCR loans are great for the long-term, refinance loan at the end of your BRRRR project. The combination of a quick and easy loan and a structure designed for rental properties makes DSCR and BRRRR the perfect pair.

Want to find out how a DSCR loan might work with your BRRRR rental? You can download our free DSCR loan calculator here. It can help you learn your ratio and get an idea of the kind of terms your property may qualify for.

Are DSCR Loans Good for Your Property?

If you’re in the market for a loan on a rental property, you can reach out to us to help with the numbers. Send us a deal or ask us a question at Info@TheCashFlowCompany.com.