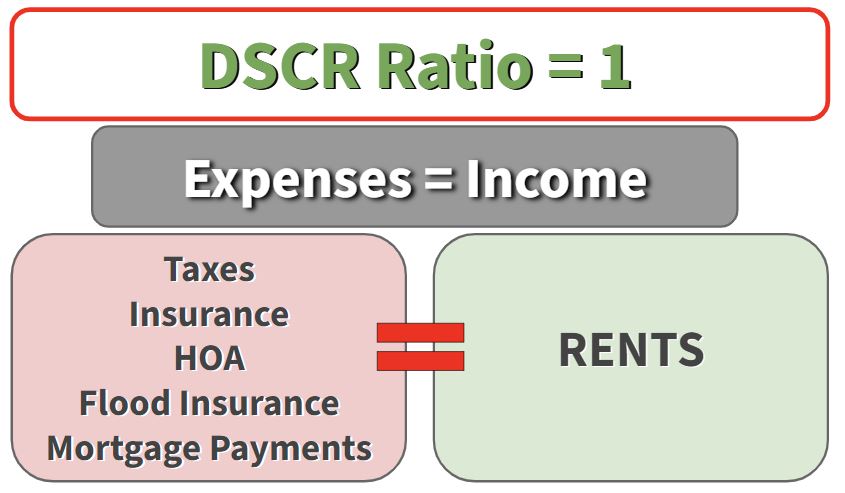

How Rising Interest Rates Impact Cash Flow

Today we are going to look at an example of how rising interest rates impact cash flow for real estate investors who are using a DSCR loan. To clarify, a DSCR loan is a loan that focuses on the rents from a rental property and the credit worthiness of the borrower. In today’s market, the increasing interest rates are truly affecting payments and more importantly they are negatively impacting cash flow.

Example:

| $250K Loan | |||

| Time Frame | Percentage | Expected Payment | Change over Time |

| Couple years ago | 3.75% | $1,158 | |

| Now | 9% to 11%

(depending on LTV) |

$2,011 | $853

Payment Increase |

| In the Future | 7%

(you refinance $2,011 principle) |

$1,663 | $348

Cash flow increase |

| The Optimus | 5%

(Looking if it dropped from 9% to 5%) |

$1,342 | $669

Cash flow increase |

This example allows us to visualize why rental properties are failing to cash flow while using a DSCR loan. As a result to higher interest rates, investors are experiencing increasing payments for their properties. This is in addition to rising taxes, and increasing insurance expenses as well. As a result, investors are struggling to break even, let alone create cash flow. In sum, all of these pressures are making it harder to be successful in real estate investing.

What’s next?

I will be doing a follow up video that will further show you the effect that interest rates have on cash flow. This will include a look from the buyers side, and how the market is going to push up your values. While we don’t have control over the interest rates, we can instead use this time to make the most of the market. By investing in undervalued properties now, you can then refinance when rates go down. This in turn will create the cash flow you need to succeed in the years to come.

Watch our most recent video about why rental properties fail to cash flow and how you can set yourself up for success by investing now.

Do you have questions about DSCR loans or how you can create generational wealth? Contact us today!