Here’s how to calculate a property’s DSCR (and what it means for your loan).

Don’t be intimidated by a DSCR loan. If the property cash flows, then you have a pretty good shot at getting approved.

And there’s a simple way to find out the cash flow of a rental property: the debt service coverage ratio.

This ratio is used by underwriters to determine if a property is positively cash flowing. It’s an important metric to understand if you want to maximize your leverage and get the most out of your investments.

Let’s go over how to calculate DSCR quickly and understand what it means for your property.

What Is a DSCR in Real Estate?

First, let’s define what DSCR is. It’s a ratio that compares a property’s income to its expenses.

You calculate DSCR by dividing the property’s income (rents) by its expenses (monthly mortgage payment, taxes, insurance, and HOA if applicable). A ratio of greater than 1 means the property is cash flowing, which is what both you and your lender want to see.

The higher the ratio, the better the cash flow, and the more money in your pocket.

For a DSCR loan, the higher this ratio is, the better the terms your loan will have.

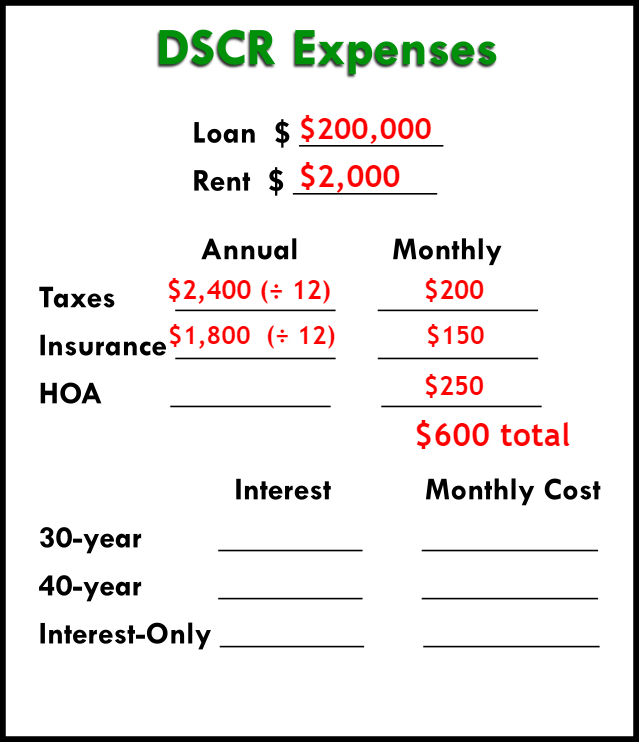

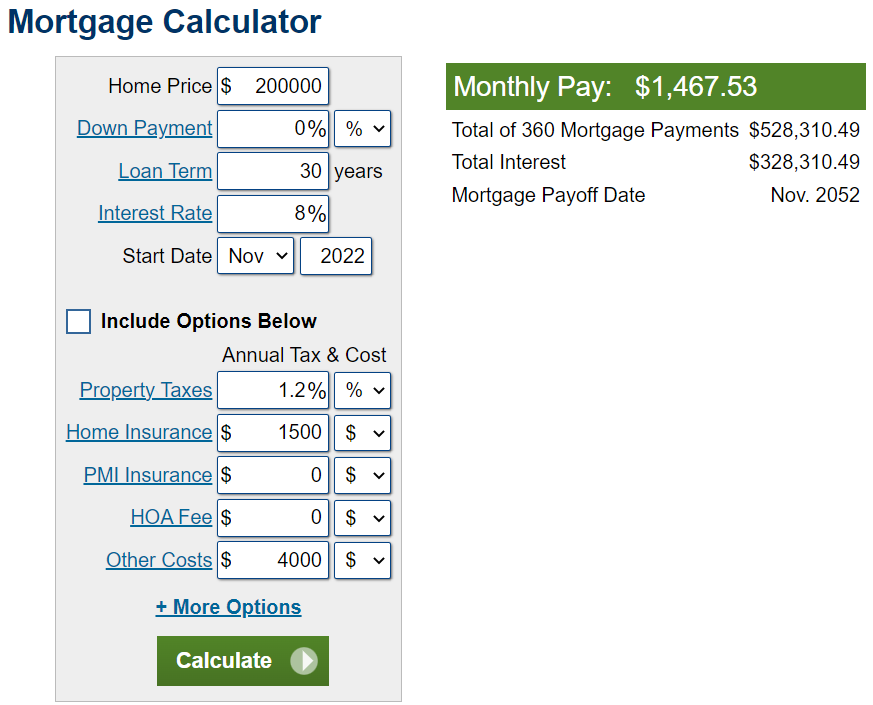

How to Calculate Expenses & Income for a DSCR Loan

To find out the expenses your DSCR loan will consider, you’ll add together four items:

- Mortgage

- Property Tax

- Insurance

- HOA Fees

To find out the income, you’ll need to check out what rents are in the area for comparable properties.

How to Calculate the DSCR

To give you a better understanding of how to calculate DSCR, let’s look at a quick example.

Let’s say we have a property with rents coming in at $1,700 a month.

The monthly mortgage payment is $1,290. Taxes are $100/ month, insurance is $100/month, and HOA is $100 /month. Added together, this gives us $1,590.

Now, to calculate the DSCR ratio, we divide the income ($1,700) by the expenses ($1,590). We get a ratio of 1.07.

This is great! The break-even point for a DSCR is a ratio of 1. Underwriters and lenders like to see a ratio of at least 1 to ensure that the property can take care of itself. Now lenders know you won’t need to take money out of your pocket to cover the expenses. This is assurance for them, making them more likely to approve the loan with good terms.

A 1.07 ratio means the property is positively cash flowing, and it’s a good investment.

Example of a Low Ratio

But what if we could only charge $1,500 in rent for this same property?

Let’s look at the impact of a decrease in rent. In this case, we’d calculate the DSCR ratio by dividing $1,500 (income) by $1,590 (expenses), which gives us 0.94. You’ll need an extra $90 out-of-pocket just to breakeven.

This is less than 1, meaning the property is negatively cash flowing.

You need to estimate the rent on a property before you think about buying it. This property at $1,500 wouldn’t be a good investment (and wouldn’t qualify for a good DSCR loan). But remember – the same property at $1,700 rent would be a good investment.

Usually, the only time DSCR loans are used on a negatively cash-flowing property is when someone gets stuck with a property they can’t sell, and a little income on the property is better than none at all. It’s not wise to purchase a rental property that you know won’t cash flow from day 1.

Negative DSCR Loans

You can still find a DSCR product for negative cash flow properties.

There are certain thresholds when you calculate DSCR loans. When you break these thresholds, you get a better rate. And better rates mean… more cash flow! Your monthly payments will lower.

Let’s go over what some of these thresholds will look like.

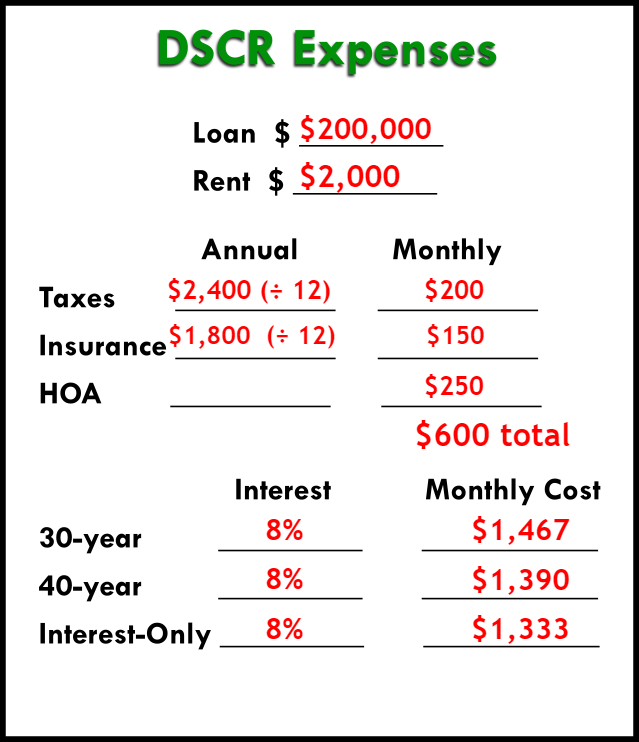

Loans for a 1.25 DSCR

Say we have a property with $1,590 worth of monthly expenses, which we can charge a $2,000 rent on. Divide the rent by the expenses, and we get a DSCR of about 1.26.

One way of thinking of this is that the property is profiting 25% over the expenses. That’s good for the underwriter (and it’s good for you).

1.25 is a threshold for DSCR lenders. In the current market at the beginning of 2022, the rate for a 1.25 DSCR is around 7.25%.

Rates for a Negative to 1 DSCR

If a property has negative cash flow, say 0.944, then the average interest rate would be 9+% on a DSCR loan.

For a breakeven ratio of 1, the typical interest rate right now would be more like 7.75%.

The Difference

Anytime you can lower the rate, that’s cash flow that goes into your pocket.

The difference between a negative DSCR and a 1.25 is about $220/month on your payment. Over the course of a year, that adds up to $2,600. If you have 5 rental properties, that’s $13,000/year. At 10 rental properties, it’s a $26,000 difference!

If real estate investing is going to be your career or retirement plan, buying properties that you know will cash flow is vital. A couple hundred bucks a month can snowball into hundreds of thousands over time.

This is why it’s important to know how to calculate DSCR quickly when you’re looking at buying a new property. Never put a contract on a rental property when you’re not sure if the cash flow fits your goals.

How to Calculate DSCR Quickly

To help keep the numbers straight when you calculate DSCR, you can download our free, simple DSCR calculator at this link.

If you have any other questions about how to calculate DSCR (or how to get a DSCR loan!), send us an email at Info@TheCashFlowCompany.com.