Today we are going to discuss the #Trick 1 you need to try before your next loan application. Are you preparing to apply for a loan? Whether it’s a DSCR loan, fix-and-flip financing, or a line of credit, there’s one simple trick to boost your credit score and secure better terms. Let’s walk through this quick, legal strategy to save you money on rates, fees, and more.

Why Your Credit Usage Matters

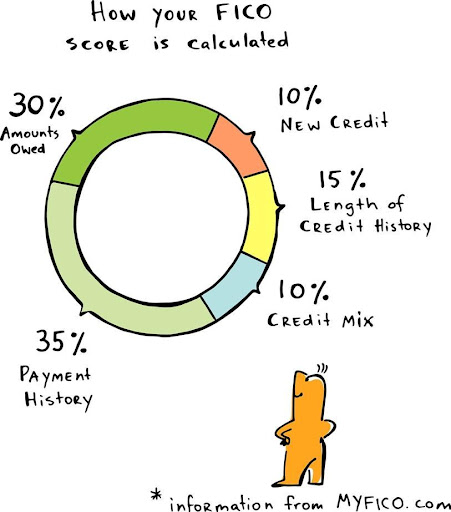

Before diving in, let’s get clear on why credit usage is key. Credit usage, or utilization, makes up 30% of your credit score. This is the balance reported to credit bureaus divided by your total available credit limit. The lower your usage, the higher your score—and that directly affects:

- Your loan-to-value ratio (LTV)

- The interest rate you qualify for

- Your overall loan approval chances

What’s the Goal?

Keep your credit usage below 30%. Anything lower shows lenders you’re financially responsible. However, avoid a 0% balance—credit bureaus prefer to see some usage.

Here’s an example:

- Credit limit: $10,000

- Current balance: $5,000

- Usage: 50% (too high!)

To hit the ideal range, bring your balance under $3,000, or 29% usage.

How to Lower Credit Usage

- Find Your Statement Dates

Check your credit card statements for the closing date. This is when your balance is reported to credit bureaus. - Pay Before the Statement Date

Pay your balances before the closing date to ensure the lower amount gets reported. - Focus on Credit-Reporting Cards

Personal credit cards and some business cards (like Capital One) report balances to credit bureaus. Use these cards strategically, or switch to non-reporting business cards to avoid usage issues altogether.

Quick Example:

Let’s say you have the following cards:

- Capital One: $5,000 balance, $10,000 limit

- Chase: $4,000 balance, $5,000 limit

- American Express: $7,500 balance, $10,000 limit

Total credit: $25,000

Current balances: $16,500

Usage: 66% (too high!)

To get under 30%, pay down:

- $2,000 on Capital One

- $4,000 on Chase

- $5,000 on American Express

New balances: $5,500

Usage: 22% (perfect!)

Why It Pays to Try This

Lowering your credit usage before applying for a loan can:

- Improve your credit score

- Qualify you for better interest rates

- Save you thousands over the loan term

For example, a DSCR loan could offer an extra point off your rate by simply boosting your score. Over a 30-year loan, that’s a huge savings!

Final Thoughts: Stay Ahead of the Game

This trick is simple but effective. Anytime you’re applying for new credit, check your usage, know your statement dates, and pay down balances early. If you’re tired of juggling personal credit cards, consider switching to business cards that don’t report to bureaus.

Want to learn more about setting up the perfect money bucket to fund your deals? Check out our guide here.

Watch our most recent video to find out more about: #Trick 1 You Need to Try Before Your Next Loan Application