How Interest-Only DSCR Loans Work

Categories: Blog Posts

Could interest-only DSCR loans be right for your properties now? Here’s how they work.

Hybrid products, like interest-only DSCR loans, weren’t as prominent three or four years ago.

But with current rates, interest-only is a strategy you need to look at in the real estate investing world.

Interest-only loans increase cash flow and leave you options for a future refinance.

Let’s look at how interest-only DSCR loans work, and what calculations you need to know.

Part One: Interest-Only

There are two parts to an interest-only loan. Part one is just interest, and part two is the paydown, or amortization.

We’ll go over the interest-only portion first.

Typically, your interest-only period is 5 or 10 years where your only cost is interest. You aren’t required to pay down the principal at all during that time. So for, say, 10 years, you pay interest, but your loan amount never goes down.

Keep in mind, with an interest-only loan, you always have the option to pay down the principal. These loans typically don’t come with a prepayment fee.

Interest-Only Example

Find the numbers relevant to your deals, and you can follow along with these calculations. You might need a loan for $500,000, or maybe just $100,000. For our example, we’ll use $300,000 as our loan amount.

The interest-only phase of interest-only DSCR loans uses one simple formula.

First, multiply the loan amount by the interest rate. This gives you the yearly interest. Divide that number by 12 (for the 12 months in a year) to get your monthly payment. The formula looks like this:

Loan Amount x Interest Rate = Yearly Interest

Yearly Interest ÷ 12 = Monthly Interest

We’ll use 8% as our example interest rate. So our equation would be:

$300,000 × .08 = $24,000

$24,000 ÷ 12 = $2,000

As long as you don’t pay down any principal during the interest-only period, your payments will be $2,000/month. This $2,000 goes directly to the bank. Your loan amount will remain $300,000, unless you choose to make an extra payment toward the principal.

Paying Principal

Every time you opt into a principal payment during the interest-only period, your monthly payment changes.

For example, let’s say you pay down $20,000 from your loan, leaving the total loan amount as $280,000. You can re-use the previous formula with this new loan amount to get your new monthly payment:

$280,000 × .08 = $22,400

$22,400 ÷ 12 = $1,866

If you chose to pay down your principal by $20,000, your new monthly payment of interest would be $1,866.

How Annual Interest Works on Interest-Only DSCR Loans

Don’t let the idea of “annual” interest trip you up. For these interest-only DSCR loans, interest isn’t calculated once from January to December. Instead, the bank will do this formula each month for your loan using your current principal.

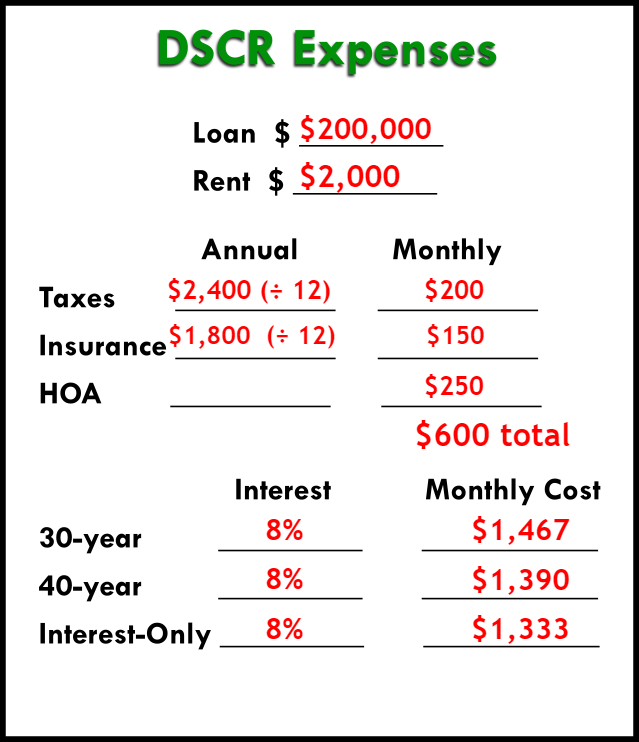

Remember that this interest is your monthly loan payment, but it is not your property’s total monthly expenses. If your loan is a DSCR, you also have to consider taxes, insurance, and HOA fees to know your actual monthly expenses.

Pros of Interest-Only DSCR Loans

There are two major advantages of interest-only loans:

- Cash Flow – Interest-only loans lower your payments, which makes for less money out and more money in. With the interest-only period, you can do deals that would never work with a typical loan payment.

- Flexible Refinance – You can refinance most interest-only loans at any time (dependent on the lender’s prepay policy). It can be a great strategy to use an interest-only loan for the next four or five years while rates are high. When rates come back down, you can refinance into another loan product that will build equity.

Part Two: The Paydown

You never have to wait to get to the paydown in order to refinance your interest-only loan. Some investors refinance the same interest-only property over and over before ever getting to the paydown part.

The interest-only portion of an interest-only loan lasts for a set number of years. For example, let’s say ours lasts 10 years.

The paydown period is when the loan starts amortizing – the actual amount borrowed starts going down. However, you’ll still need to pay normal interest along with the principal payment.

With most lenders, you’ll get either a 30-year or 40-year loan. A 30-year interest-only loan would involve 10 years of just interest, plus 20 years of paydown. For a 40-year, you’d have 30 years’ worth of amortization payments.

A 30-year loan’s payments will be higher because you’re paying the same amount off in a shorter period of time.

Calculating a Paydown Payment Example

Let’s break down the difference between a 30-year and 40-year interest-only loan.

30-year loan = 10 years interest, then 20 years of amortization

40-year loan = 10 years interest, then 30 years amortization

You can use an amortization calculator tool to figure your monthly payments for the paydown period.

Let’s look at an example for a $300,000 interest-only loan. The paydown period payments would be:

30-year = 10 years of $2,000/month + 20 years of $2,509/month

40-year = 10 years of $2,000/month + 30 years of $2,201/month

Remember that you’re never locked into paying a full interest-only loan. An interest-only loan may be worth looking into for your property. Especially if you need a product with lower monthly payments while you wait out rising interest rates.

Help with Interest-Only DSCR Loans

Have questions about interest-only DSCR loans? Is there a deal you’d like us to take a look at?

We search hundreds of loans every month – now is a great time of variety in loan products. We’d love to help you find exactly what you need.

Email us at Info@TheCashFlowCompany.com.