How Can I Qualify for a Loan for My Real Estate Investments?

Today we are going to answer one of the biggest questions that real estate investors have, “How can I qualify for a loan for my real estate investments?” Thankfully there are a multitude of products available for investors to not only purchase new properties, but to refinance as well. Whether or not you have a job, just changed jobs, or write everything off on your taxes, there are products out there for you. What are your options and how do you get started? Let’s take a closer look!

Your best loan option!

One of the most versatile loan options available for investors is a DSCR loan. A DSCR loan is only available to investors and stands for the debt service coverage ratio. How do you qualify? As long as your rental property will cover the debt, you will be able to qualify for a DSCR loan. Unlike traditional loans, a DSCR loan will not take into consideration when you started your job or how long you’ve been self-employed. Instead, the lender’s primary focus is whether or not the income from the property qualifies for the loan.

What does DSCR mean?

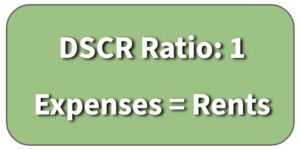

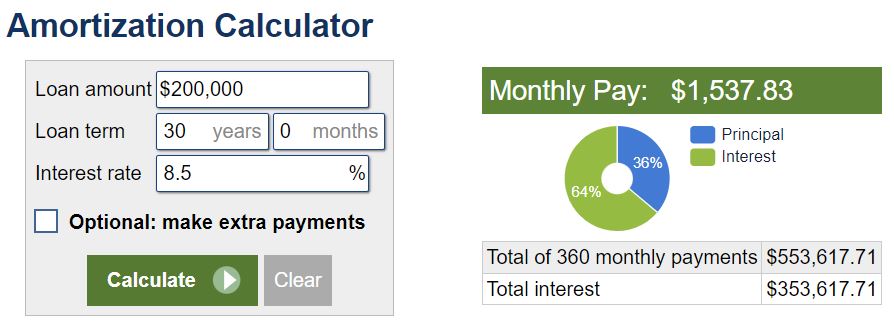

The debt service coverage ratio is where your property breaks even. Just to clarify, that is when the income from the property and the expenses break even. While every property has a different break even point, this is the value that lenders will be looking at to determine whether or not the property qualifies for a DSCR loan. The expenses that lenders take into consideration are the mortgage payment (including interest), taxes, insurance, flood, and HOA. For example, if your rent is $1,000, then your expenses need to be $1,000 or less in order to qualify for a DSCR loan. The best scenario would be if your rents were $1,500 and the expenses were $1,000. This would create a $500 cash flow for the property.

Find the versatility you need to succeed.

Nowadays, DSCR loans are not only for 1 to 4 unit properties. Instead DSCR loans can cover 8 to 10 unit properties and even mixed use properties! That’s not all! There are also a lot of refinancing options available for investors who want to get cash out of their properties. Don’t miss out on this best kept real estate secret! Find the best product today that not only provides ultimate flexibility but meets all of your investment needs as well.

Contact us today!

Here at The Cash Flow Company we are happy to run through the numbers with you to see what product is best for you. Contact us today to find out more about how you can qualify!

Watch our most recent video: How Can I Qualify for a Loan for My Real Estate Investments?