How to Calculate Your Maximum DSCR Loan Amount

Categories: Blog Posts

How to Calculate Your Maximum DSCR Loan Amount

Today we are going to go over how to calculate your maximum DSCR loan amount. Most DSCR loans are based off of LTV. Just to clarify, LTV is normally 75% for rate and term and 80% for purchase. However, there is another factor that you need to take into consideration. That factor is the break even point. The break even point can either limit how much you can get out of the property, or make you put more money in at purchase. Let’s take a closer look at the numbers to ensure that you can calculate your maximum DSCR loan amount prior to purchasing a property.

What do you need to know before purchasing a property?

Many investors use the BRRRR strategy when investing in real estate properties. While this is an excellent method to use to build a portfolio, investors are often faced with issues when it comes to refinancing the property. While investors expect to refinance out at 75% to 80%, it doesn’t always work as planned. This is due to the fact that the DSCR ratio comes into play. The DSCR ratio can limit the amount that you can get out of the property. That is why it is important to know your numbers before purchasing the property or prior to refinancing. By calculating the break even point on your DSCR ratio you will be able to create the cash flow you need to succeed.

Example: Calculating how much you would qualify for.

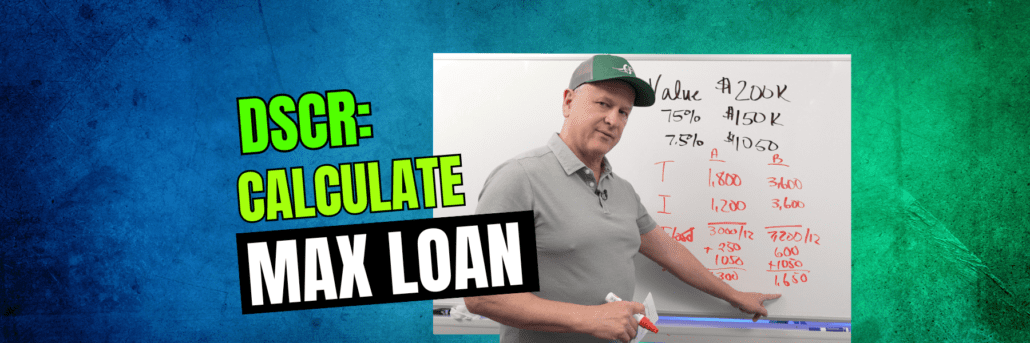

Value of the property is $200K

Refinance is 75% rate and term

$200K x .75 = $150K (this is the loan amount you would qualify for)

Keep in mind that this example is with a good credit score and a good rate at 75%.

Example: Calculating monthly payment.

At 75% we are going to use a 7.5% rate.

$150K x .075 = $1,050 monthly payment (includes principal and interest)

If we have the same property in a different area, different zip code, or different state, then this property may or may not qualify for the 75% loan.

Example: One property qualifies and one does not.

It is important to take everything into consideration when determining whether or not the property qualifies. The numbers that you need to consider include taxes, property insurance, flood insurance (when applicable), and HOA (when applicable). Remember, in order to qualify would mean that the rent needs to be greater than or equal to the expenses for the property.

| Property A | Property B | |

| Taxes: | $1,800 | $3,600 |

| Property insurance: | $1,200 | $3,600 |

| Flood insurance: | $0 | $0 |

| HOA: | $0 | $0 |

| Total | $3,000 | $7,200 |

| Monthly amount | $3,000/12 months = $250 | $7,200/12 months = $600 |

| Break even point (mortgage payment + taxes and insurance) | $1,050 + $250 = $1,300 | $1,050 + $600 = $1,650 |

| Rent is $1,400 a month | This property will qualify for the full $150K refinance | This property will NOT qualify for $150K because the rent is less than the break even point |

In this example it is clear to see that even though you qualify for the DSCR loan, the property doesn’t always qualify. This example is all based on the DSCR ratio and shows how the income and expenses compare. Keep in mind that every property will be different and every location will be different as well.

In conclusion,

Before you purchase a property or get into BRRRR make sure that you run the numbers to determine if the property breaks even. This is done by finding out what the rents are for similar properties in the area, along with collecting quotes for the taxes and insurance on the property. In doing so, you will be able to ensure that the property is going to hit the LTV that you want when refinancing.

If you have any questions or want to run through some numbers reach out to us! We are happy to work through the numbers with you to ensure that the property will be a good investment.

Watch our most recent video How to Calculate Your Maximum DSCR Loan Amount to find out more!

")

")

")

")