How can real estate investors WIN in the changing 2024 market?

We’re expecting to see more foreclosures and more properties available at discounts in the coming year which is ideal for real estate investors in the business of fix and flips and rentals.

No matter where you came from or whether you have a college degree, anyone with the willingness to work and learn can make good money in real estate.

We’re here to share a few tricks so that, as opportunities show up in the coming year, you’re set for success.

Preparing as Real Estate Investors

There are typically two sides of real estate investing: 1) finding good properties and 2) financing.

As we said before, you need money to make the money. Today, we want to look at the financing side of things so you’re ready when the good properties show up.

As an investor, it’s important that you’re attractive to lenders. Lenders, as a rule, want to lend you money, but it’s important to understand what they’re really looking for as well as how you can diversify your money bucket to maximize your success.

Filling Your Real Estate Money Bucket

For any project you do, you need money. We refer to this collection of money as your money bucket.

The money in your bucket comes from two sources: 1) a lender and 2) you.

Both of these areas of funding are going to come together and fill the bucket to finance your project.

1. Be Honest With your Lender and Get Your Projects Done

This may seem obvious, but make sure you’re honest with your lender.

Make sure you’re upfront about your financial history. It should go without saying, but don’t try to hide that you’ve had a bankruptcy or defaulted on a loan in the past.

If you’re concerned about your financial history, trust us: It’s much worse to hide it and make the lender find out on their own (which they will).

Once they find out, it will be harder for you to get a loan. And if you do find a loan, your options are going to be severely limited—not just because of the history, but even more so because you hid important information.

Options are super important for real estate investors.

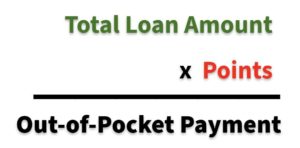

Options drive down the costs of loans, and anytime you pay less for money, the more money there’s going to be in your bucket.

Similarly, when you say you’re going to get a project done, get it done. Whether it’s a flip or a BRRRR, construct a solid timeline on the front end so you and your lender are on the same page.

It’s often a good idea to put in a bit of a cushion when talking to your lenders so that you don’t panic if there are minor delays in your project.

Lenders want to see honest people who are doing their best. Most lenders are happy to support honest investors who are upfront with them with more money, more funding, more options.

2. Your Credit Score Matters

The better your credit, the more options you’ll have.

Impact of Credit: Banks love clients with high credit scores. The higher the score, the more options they’re likely to offer.

As with finding a loan, the more options banks offer, the more likely you are to find a great deal.

Personal vs. Business cards: Using personal credit for investing can quickly turn into a problem.

Using personal credit cards or lines of credit for business projects can drive people’s scores down.

We strongly recommend using business credit cards for your real estate investing. You should still make sure you’re paying everything on time, but that business credit card in your name isn’t going to be reported on your personal credit report.

This keeps your credit score higher as you’re looking for loans.

Lines of Credit: Having a variety of credit lines, and opening those strategically, helps real estate investors fill their money buckets. Lines of credit in business credit cards, HELOCs, etc. can get you more prepared for down payments, earnest money, repairs, and more.

It’s helpful to have backup lines of credit that are ready for when you need money for time-sensitive deals.

Fill your bucket and your options.

3. Finding Real People’s Money as Real Estate Investors

When trying to fill your money bucket, you shouldn’t overlook your friends and family.

Look out for real people in your life who are willing to invest in your project. Even if they only want to invest $10K, that can still help you cover your earnest money or smaller payments.

A lot of people are looking for private investments that offer better returns than traditional banks. Working with the real people in your life can make a huge difference in your ability to fund your project.

If you need help with navigating those personal investments, we’re happy to help. We have a lot of experience working with diverse money buckets and know how to keep notes for your financial records so those private loans are correctly accounted for.

Calling All Real Estate Investors: Prepare for 2024!

It’s important in 2023 to get ready for what’s coming in the future.

Make sure you have lenders set up from hard money to neighbors and everyone in between. Check your credit scores now to ensure you have the options that will make your investing a success.

You can also check out our free and easy tools to help get you ready for the upcoming market. We even have a free credit score checklist for you to use.

As always, we’re always happy to help! If you have any questions about the upcoming market, your loan options, or how to fix your credit, reach out to us at Info@TheCashFlowCompany.com.

You can also check out our YouTube channel to learn more about real estate investing.