What are DSCR prepay penalties and how can you navigate them?

One of the normal things you’ll come across when looking at DSCR loans are prepay penalties. Understanding how they work (and the options you have) can help you make the best choices for your project.

What are DSCR Prepays?

If you’re working with a DSCR or a non-QM investor, you’re likely going to find lenders charging prepay penalties.

Typically, if you want to exit the loan within a certain time period—often three to five years—they’ll charge an additional exit fee. This means that if you pay off your loan early, you could run into what’s called a hard prepay.

Understanding the Cost of Prepay Penalties

Lenders don’t care about why you’re paying off your loan early. If you pay them in full, they’re going to charge the agreed upon fee (the prepay penalty).

For example, if you have a $100K loan with a 3% prepay penalty, you would pay them 3% of the $100K on top of the principal and any interest or other fees owed.

While this can feel frustrating, these penalties actually allow these lending institutions to keep money flowing. A prepay helps them keep interest rates stable by ensuring a consistent flow of capital.

Different Prepay Options for DSCR Loans

DSCR loans offer two standard prepay options: five-year or three-year periods.

How does this connect to DSCR prepay penalties?

During the initial five- or three-year period of your mortgage, you will be penalized for paying off your loan before the prepay period has elapsed. If you keep your loan past that benchmark, you will have no more prepay penalty.

You typically will find two basic types of prepays:

-

Straight Prepay: If you have a straight prepay, a lender may charge you a fixed percentage of the principal balance for each year, regardless of when you pay off the loan.

-

Declining Prepay: A declining prepay is exactly what it sounds like. Each year, the prepay penalty decreases. For example, it may be 5% of the principal balance the first year, 4% the next, etc. until the prepay penalty disappears altogether.

Choosing the Right Option for You

How can you choose the right DSCR option for your project?

It’s important to look at the prepay penalties of your loan so that you can figure out what fits your particular investment. You should also take time to research the following to make sure you’re getting the best deal possible:

Think about your timeline.

Are you keeping the property long term? Do you think the market’s going to go down? All those things come into play when you’re determining what prepay is best for you.

A good lender will walk you through the numbers and your options, but the more information you have about your timeline, the better they’ll be able to help you.

Work with a knowledgeable lender.

Make sure you pick a lender who has options. DSCR companies often specialize in loans for a specific group, so it’s possible they won’t have the perfect loan for you.

A good lender should have at least five to ten different DSCR funders that they could match with your loan. They should be able to help you find a loan that fits your timeline, cash flow, and specific project needs.

Consider your exit strategy.

Prepay penalties come into play when you exit your loan.

If you know on the front end of your project that you want a DSCR loan but might not need five years to complete it, then that should be a huge consideration when configuring your DSCR.

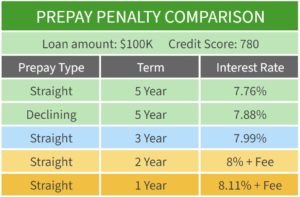

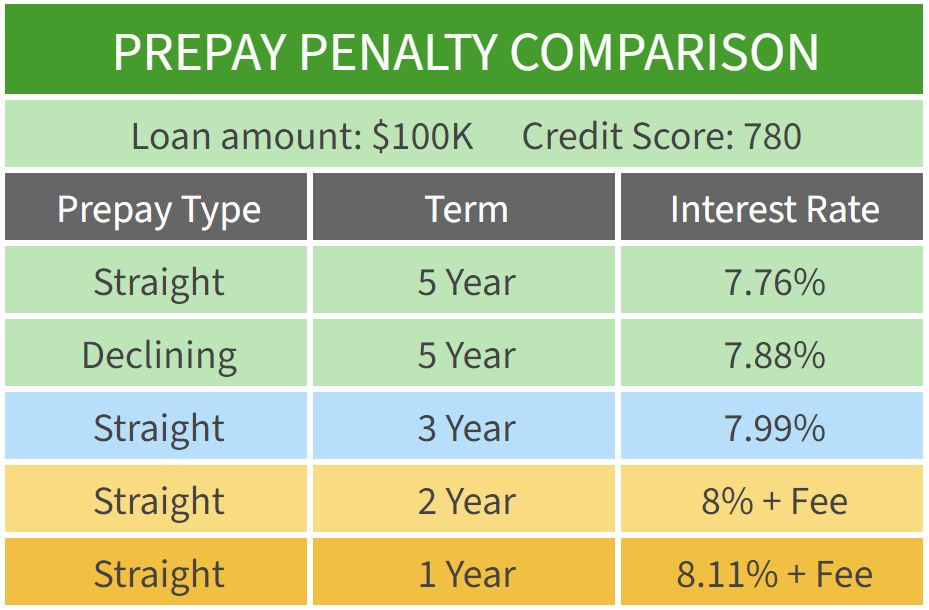

Prepay Cost Examples

This chart can help you understand how DSCR prepay penalties can affect the cost of your project.

In this example, we’re considering a loan of $100K from a person with a 780 credit score.

When comparing straight vs. declining prepay options, it’s always worth considering the timeline of your project as well as whether or not interest rates are projected to drop.

Also, always check what added fees your lender might have connected with their prepay penalties as these can vary significantly.

How We Help

Sometimes it can be difficult to find lenders who will take the time to run through all the numbers with you. You’re welcome to contact us at Info@TheCashFlowCompany.com and we will be happy to walk you through your options.

You can also visit our website to learn more about real estate investment or to find tools such as our free and easy DSCR calculator.

As always, we’re more than happy to look at your project and help you figure out a deal that works for you.