Investor Mortgage Report 4.14.2020

Categories: Blog Posts, Resources, Tips, Trends Tuesday

Why did all the banks just make it damn near impossible to get a loan on an investment property?

For lenders, times are more uncertain than ever.

With conventional/standard loans as the only lending option available for rental investors, lenders went and changed the rules…and not in the investor’s favor.

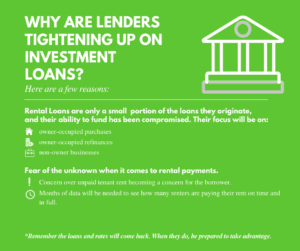

As of this week, the new underwriting criteria has hit 90% + of the market for investor loans on rental properties. Plus, most lenders now require a minimum of 6 months reserves (and, a lot of times, up to 12 months) for every rental property that has a loan on it. That’s right. If you have four rental properties, you now need at least 6 months of payment reserves on each property. That adds up quickly.

That may not even be the worst of it.

In addition, most lenders are not allowing borrowers to use the rental income from their properties to qualify. If they do, they might only allow a very low percentage of the rent (like 50% of gross rent). That means if you have rent coming into a property at $2K, they may only count 50%, or $1K, of that towards your expenses (if they allow you to use it at all). In this example, if the rental property has expenses at or above $1K (and most will) the underwriters will expect you to cover the shortage with other non-rental cash flow.

So, if you don’t have great credit (lenders have raised the threshold here, too) and other income to qualify for a new loan, you will be out of luck…for now.

We don’t know how long this will last. It might be weeks, but more likely months. Nobody will know until banks and lenders figure out how current stay at home orders will affect the markets.

So, why exactly is this happening?

Once the lenders get the data, they will adjust. Let’s cross our fingers that rents are being paid and, likewise, mortgages are kept up. This flow of money will help bring lenders and loan choices back to our market.

What can you do?

- Keep informed on what is happening in the lending markets. If you are selling properties, then stay updated for your potential buyers, too.

- Keep paying your mortgages. This will help the overall market, but especially you when you are looking to borrow in the future for better rates (the rates are expected to be great after we return to some normal) or new opportunities.

- Keep your credit score high and keep working with your renters to pay what they can when they can.

Remember the loans and rates will come back. When they do, be prepared to take advantage.

If you have a credit score at or above 760, and have ability to income qualify, then your rate estimates this week for conventional loans look like the following:

- Paying closing costs rates for rental properties (1-4 units) in the high 3’s for a rate and term. Typical break-even point is between 2 and 2.5 years.

- Paying little to no closing costs rates are high 4’s (best for strategies for keeping a property under 2.5 years).

If you want to know where you stand and what you can do, schedule a time to discuss your lending needs with us today by emailing mike@thecashflowcompany.com.

")

")