Today we are going to look at an example of how rising interest rates impact cash flow for real estate investors who are using a DSCR loan. To clarify, a DSCR loan is a loan that focuses on the rents from a rental property and the credit worthiness of the borrower. In today’s market, the increasing interest rates are truly affecting payments and more importantly they are negatively impacting cash flow.

Example:

$250K Loan

Time Frame

Percentage

Expected Payment

Change over Time

Couple years ago

3.75%

$1,158

Now

9% to 11%

(depending on LTV)

$2,011

$853

Payment Increase

In the Future

7%

(you refinance $2,011 principle)

$1,663

$348

Cash flow increase

The Optimus

5%

(Looking if it dropped from 9% to 5%)

$1,342

$669

Cash flow increase

This example allows us to visualize why rental properties are failing to cash flow while using a DSCR loan. As a result to higher interest rates, investors are experiencing increasing payments for their properties. This is in addition to rising taxes, and increasing insurance expenses as well. As a result, investors are struggling to break even, let alone create cash flow. In sum, all of these pressures are making it harder to be successful in real estate investing.

What’s next?

I will be doing a follow up video that will further show you the effect that interest rates have on cash flow. This will include a look from the buyers side, and how the market is going to push up your values. While we don’t have control over the interest rates, we can instead use this time to make the most of the market. By investing in undervalued properties now, you can then refinance when rates go down. This in turn will create the cash flow you need to succeed in the years to come.

Watch our most recent videoabout why rental properties fail to cash flow and how you can set yourself up for success by investing now.

Do you have questions about DSCR loans or how you can create generational wealth? Contact us today!

DSCR Loan: Why Rental Properties Fail to Cash Flow

Today we are going to dive into an example illustrating why rental properties fail to cash flow using a DSCR loan. A DSCR loan are loans focused on the rents from a rental property and the credit worthiness of the borrower. In today’s market, the increasing interest rates are truly affecting payments and more importantly they are impacting cash flow. As a result, it has become harder and harder to qualify for a DSCR loan. Likewise, DSCR ratios are changing also. What used to be a 1:1 ratio (rents compared to expenses), has now increased depending on your LTV. Therefore, many investors can no longer qualify because there is no cash flow for the property. So, what does this look like numbers wise? Let’s take a closer look.

Example:

$250K Loan

Time Frame

Percentage

Expected Payment

Change Over Time

Couple years ago

3.75%

$1,158

Now

9% to 11%

(depending on LTV)

$2,011

$853

Payment Increase

In the Future

7%

(you refinance $2,011 principle)

$1,663

$348

Cash flow increase

The Optimus

5%

(Looking if it dropped from 9% to 5%)

$1,342

$669

Cash flow increase

In this example it is clear to see why rental properties fail to cash flow, especially with a DSCR loan. The increasing rates have caused payments to increase as well. When combined with ever rising taxes and insurance expenses, investors are struggling to break even, let alone create cash flow. All of these pressures are making it harder to be successful in real estate investing.

Why is it a good time to buy?

So, why is it a good time to buy? My suggestion for investors is that they need to find something that has good equity and at 25% to 30%. As long as it is breaking even, then in a year or two when rates go back down, you will be able to refinance to increase your cash flow without buying another property. The more affordable the homes are, the bigger the market becomes. The good news is that buyers are going to start buying again, and the values around you are going to increase.. While no one can predict that the interest rates will go back down to 2.5% for owner occupied and 3.75% for investors, there are indications that interest rates will drop in 2024.

What’s next?

I will be doing a follow up video that will further show you the effect that interest rates have on cash flow. This will include a look from the buyers side, and how the market is going to push up your values. If you can find a good undervalued property now, then you are going to not only create cash flow, but create generational wealth as well. You’re not alone! There are a lot of people who are questioning if they should buy now.

Watch our most recent video about why rental properties fail to cash flow and how you can set yourself up for success by investing now.

Do you have questions about DSCR loans or how you can create generational wealth? Contact us today!

What do you need to know about your DSCR loan so your investing is easy, lucrative, fun, and fast?

We want to give you the tools you need to win in the real estate game.

In a recent article, we learned how lenders look at your credit score to determine the maximum loan they’ll offer. Today, we want to apply the same principles specifically to DSCR loans.

Some investors focus on fixing and flipping properties, while others create wealth through rentals. DSCR loans are one of the most useful tools for investors that are specifically designed for rental properties.

Understanding Leverage

Leverage is what we call using other people’s money. This typically comes in the form of bank loans, but it’s not limited to that.

Things like financial gifts, small loans from friends and family, your credit score, and loans from companies like Hard Money Mike can all give you leverage.

This leverage creates an equal playing field in the investing world. You don’t need to be wealthy to use leverage well.

Credit Score as Leverage

In this day and age, credit scores matter a lot. A good credit score is a powerful tool that you can use to increase your leverage.

We also sometimes talk about money buckets. Your ‘money bucket’ is the money you bring to the table. Obviously, if you’re a newer investor, your money bucket might not have as much personal money to fill it, in which case credit score matters even more.

However, strategically using your credit score, credit cards, business cards, HELOCs, etc. to fill your money bucket now is a great way to make sure you’re ready for future investing.

How Does Credit Score Impact a DSCR Loan?

DSCRs are investor-friendly loans. Banks calculate these loans based on the break-even point between the income of the property (rents) and the payments for that property (taxes, insurance, HOA, etc.).

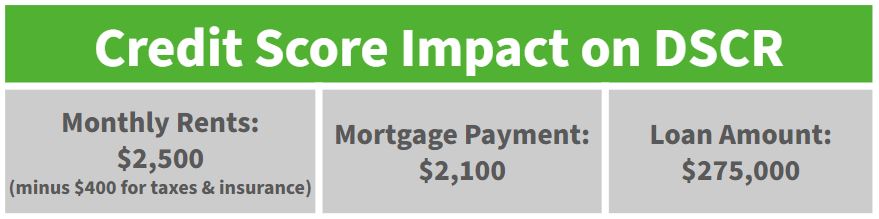

Let’s look at an example to see how credit score can impact your DSCR loans:

Once you subtract your expenses from the monthly rent, you’re left with $2,100. This means that, in order to maintain a DSCR ratio of 1 (the minimum to break even), you need a loan that has monthly payments of $2,100 or lower.

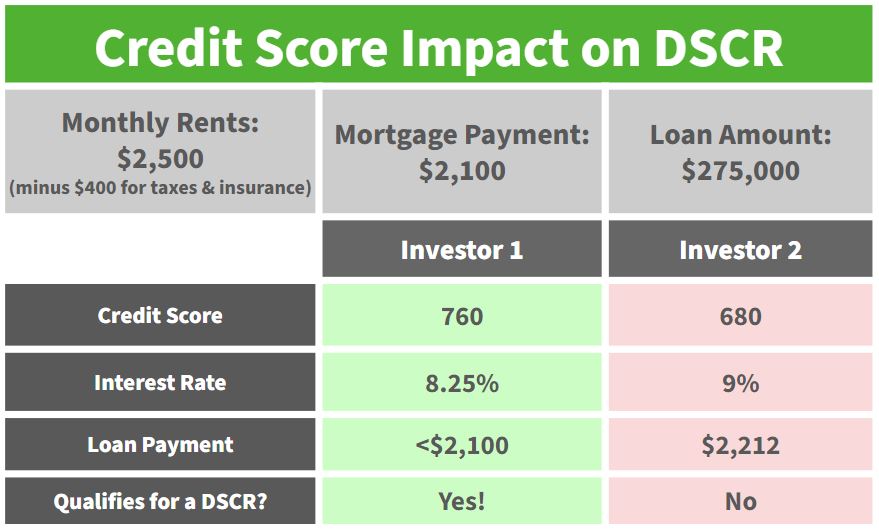

In the following example, Investor 1 has maintained a high credit score while Investor 2 has dipped below most banks’ minimum requirements.

In the two examples above, everything is the same except for the credit scores, and the effect is significant. Investor 2 can’t get a loan to refinance, and they’re either going to have to sell the property or keep their original loan for far longer than they wanted.

Regardless, the person with the higher score is able to move through the investing process easily, lucratively, and quickly.

A bad credit score can tank your leverage and sabotage your investing by creating unnecessary roadblocks for your projects.

How to Fix a Bad Credit Score

In the example above, Investor 2 struggled with a usage issue. This means that, even though they paid off their balance on time every month, excessive use of their personal credit card ended up driving down their score.

Here’s the deal: personal credit cards are not built to handle consistent real estate investing expenses. If you’re doing consistent real estate investing, we recommend looking into business credit cards.

Business cards often have higher usage limits which are ideal for the constant wear and tear of this industry.

You can also look into secured usage loans as a way to quickly boost your credit score.

Main DSCR Loan Takeaways

Leverage is king, and credit scores are an important piece of your leverage.

A good credit score makes it easier for you to qualify for and refinance your DSCRs. They can also help you put less money down on a property and increase your cash flow.

Take care of your money buckets and credit score on the front end so you can succeed when deals come your way.

If you’re interested in learning more about how you can E.L.F.F. your investing, feel free to reach out to us at Info@TheCashFlowCompany.com or fill out a contact card.

Getting a DSCR loan can be not only easy but rewarding as well. If you want to close a real estate deal fast and easy, simply follow these three simple steps. Begin by answering these questions, and you’ll be on your way to getting a loan that’s perfect for you and your cash flow.

Step 1: Check Your Rent Coverage

First, ask yourself: does your rent cover all your costs? This includes:

Mortgage payment

Taxes

Insurance

HOA fees

While it’s not always necessary, having your rent cover these costs can help you get better rates as well as higher loan-to-value products. At the very least, aim to charge rent that covers your monthly payments. However, if your rent does cover these costs, then you’ve passed the first step!

Example: Imagine you own a rental property. Your mortgage payment is $1,200, your taxes and insurance are $200, and your HOA fee is $100. Your total monthly cost is $1,500. If you charge $1,600 in rent, you cover all your costs and even make a little extra.

Step 2: Review Your Credit Score

Next, consider your credit score. You can get a DSCR loan with a score in the low 600s, but it will cost you more. Therefore a lower credit score can add up to one or more percentage points to your interest rate. This in turn can increase your monthly payment by $200 to $400.

Example: Let’s say you have a credit score of 620. You might get a loan with a 7% interest rate instead of 6%. On a $200,000 loan, that extra 1% could mean paying $2,000 more per year in interest.

If you need tips to raise your score, check out resources like our YouTube channel for advice on improving your credit.

Step 3: Choose the Right Lender

Finally, work with a lender who offers many options and programs. Every mortgage company has an ideal client, and you want to make sure your lender has an option that fits your needs at the lowest cost.

Example: You find a lender who offers various DSCR loan programs. One program might have a lower interest rate but higher fees, while another might offer a higher interest rate but lower closing costs. Choosing the right program can save you money and boost your monthly cash flow.

Conclusion

And that’s it! Those are the three key questions you need to answer before diving into a DSCR loan. If you find any step challenging, don’t worry. Our team is here to help you. We’re eager to set you on a path that helps you make the money you need to live the life you want.

Watch our most recent video to find out more about: How to Get a DSCR Loan in 3 Steps

https://thecashflowcompany.com/wp-content/uploads/2024/06/Blog-Image-Template-Kira-98.png6001800The Cash Flow Companyhttps://thecashflowcompany.com/wp-content/uploads/2022/09/The-Cash-Flow-Company-logo.pngThe Cash Flow Company2023-10-10 09:00:322024-06-21 23:33:27How to Get a DSCR Loan in 3 Steps

DSCR Loan – Is It Right For Your Real Estate Investment?

What is a DSCR Loan?

A DSCR loan stands for Debt Service Coverage Ratio loan and is an excellent loan for real estate investment. It’s designed specifically for real estate investors. This type of loan helps you buy rental properties, whether they are long-term or short-term rentals. It’s not for flips or homes you plan to live in.

Why Choose a DSCR Loan?

Choosing a DSCR loan can be a smart move for several reasons:

Easy Qualification: You don’t need to worry about how long you’ve been in business or your personal income. Even if you started your business yesterday, you could qualify.

Focus on Property Income: The loan qualification is based on the income generated by the property, not your personal income.

30-Year Loan Options: You get a good 30-year loan product, which can provide stability and predictability.

How Does a DSCR Loan Work?

The key to a DSCR loan is that it focuses on the property’s ability to generate enough income to cover its expenses. Here’s how it works:

Property Income: The income from the rental property should at least cover the mortgage, property taxes, insurance, and any HOA or flood insurance fees.

Credit Score: Your personal credit score is important. The higher your score, the better the terms and rates.

Loan-to-Value Ratio (LTV): This is the amount of the loan compared to the property’s value. Lower LTV means less risk for lenders and better terms for you.

Who Can Benefit from a DSCR Loan?

DSCR loans are perfect for:

New Investors: If you’ve just started your real estate investment journey, you can qualify even without a long business history.

Tax Savvy Investors: If you write off a lot of expenses on your taxes, which can reduce your reported income, this loan can still work for you.

Expanding Portfolios: Investors looking to add more rental properties can benefit from the flexible qualification criteria.

Example

Imagine you are an investor who just started a year ago. You found a great rental property, but traditional lenders won’t approve your loan because you don’t have two years of business income. A DSCR loan can help. As long as the rental income covers the mortgage and other expenses, you can get the loan and grow your investment portfolio.

Important Considerations

Before jumping into a DSCR loan, consider these factors:

Prepayment Penalties: These loans often come with penalties if you pay them off early. Make sure to understand these terms before committing.

Higher Interest Rates: DSCR loans can have slightly higher interest rates compared to traditional loans. This is because they are easier to qualify for.

Not for Flips or Personal Use: These loans are strictly for rental properties, not for homes you plan to flip or live in.

Is a DSCR Loan Right for You?

If you’re a real estate investor looking for a flexible loan option that doesn’t rely heavily on your personal income, a DSCR loan could be the perfect fit. It’s especially useful if you’re new to the business or if you maximize your tax deductions. Always run the numbers and shop around for the best terms.

Get Started with a DSCR Loan Today

A DSCR loan is an excellent loan for real estate investors. Is it right for your investment needs? Contact us at The Cash Flow Company. We have the tools and expertise to help you understand your options and find the best loan for your needs.

Watch our most recent video to find out more about: DSCR Loan – Is It Right For Your Real Estate Investment?

https://thecashflowcompany.com/wp-content/uploads/2024/06/Blog-Image-Template-Kira-88.png6001800The Cash Flow Companyhttps://thecashflowcompany.com/wp-content/uploads/2022/09/The-Cash-Flow-Company-logo.pngThe Cash Flow Company2023-09-29 09:00:542024-06-17 23:17:55DSCR Loan – Is It Right For Your Real Estate Investment?

If you’re new to investing in rental properties, understanding how DSCR loans work is essential.

In the investment world, rental properties are a great source of wealth. The financial potential in fixing up places to then rent out is a very lucrative model, especially in the current housing economy.

What is a DSCR Loan?

DSCR loans are specifically designed for real estate investors who hold rental properties.

The acronym literally stands for Debt-Service Coverage Ratio which is a fancy way of saying that the loan cares about the cash flow of a property.

The great news, especially for new investors, is that accessing these loans is less dependent on personal or business income. Even if you’ve just begun a new business, qualification for DSCR depends almost entirely on the potential value and expenses of the rental property itself.

What is a DSCR Ratio?

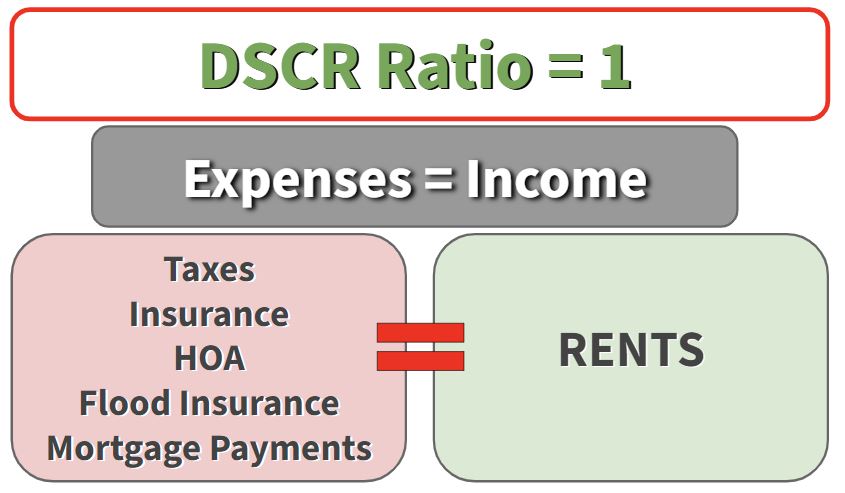

The DSCR ratio is a simple calculation that compares income to expenses—the cash flowing in vs. the cash flowing out—on a single property.

Essentially, a DSCR ratio of 1 simply means that the income and expenses equal each other.

The DSCR ratio measures the break-even point of your investment. So long as you bring in the same amount of money as you invest, you won’t lose anything.

However, a DSCR ratio of higher-than-1 is even better. A higher ratio means that you’re bringing in more money than you’re spending—generating cash flow and building wealth.

Use Our DSCR Loan Calculator

To help you find your projected rents, expenses, and ratio, you can use our DSCR loan calculator. It’s a free, user-friendly download that will help you estimate your DSCR ratio to see if your investment property is going to break even.

Once you have an estimate for your ratio, it’s time to start looking for loans.

Finding a DSCR Loan

Banks typically like to see ratios of 1 or higher.

However, if you’re investing in rental properties that might not break even, you can often still find a loan, but you might be stuck with higher rates.

How can your credit score impact DSCR loans in the real estate investing world?

Credit score impacts investors potentially more than anything else. Lenders will adjust the rates and terms of loans based purely on the three digits of credit score on a person’s financial records.

Leverage is the key to successful real estate investing, and understanding the impact of credit score is a critical facet of that leverage.

This article uses real-life examples to illustrate the difference a good credit score makes in the investment world.

How Can Credit Score Impact DSCR Loans?

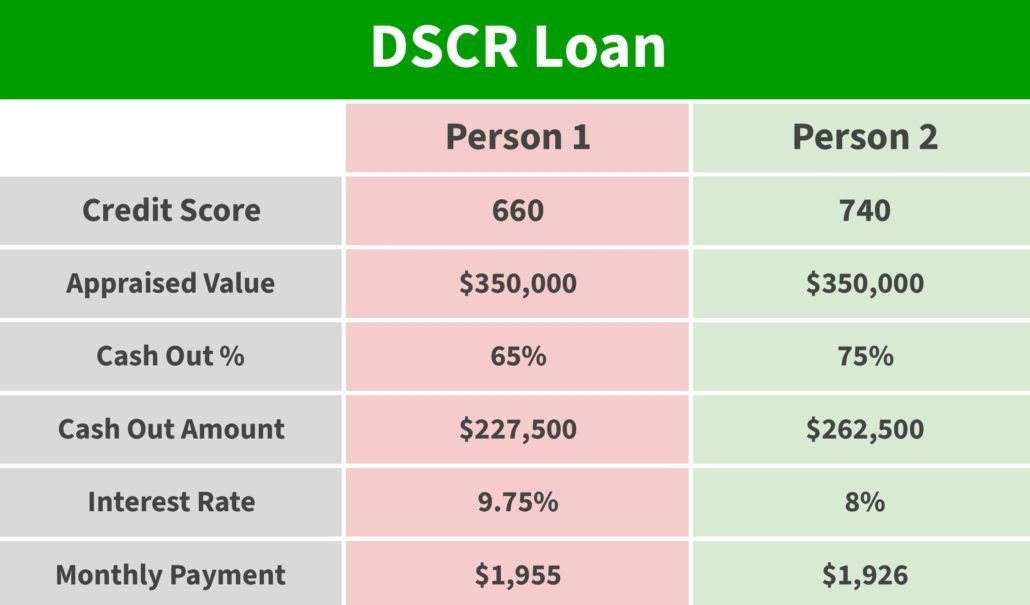

Let’s look at how DSCR loans can be impacted by a low credit score using two example clients:

One (Person 1) has a low credit score of 660

The other (Person 2) has a high score of 740

We see a lot of clients looking at cash out refinancing, so we’ll look at that type of project.

What’s the Difference?

If Person 1 has a 660 credit score, not only will they likely struggle to find lenders, but 65% is about the best they could look for. This directly translates into less money out of that property.

In contrast, Person 2 with a 740 score should be able to fairly easily get 75%. The more money out, the better your leverage.

As you can see in the chart above, not only does the person with a lower credit score get less cash out, but their rate is also higher which raises their monthly payments.

Credit Score Matters

Although at first glance, it’s tempting to just look at the monthly payments and think, “It’s not that big of a difference,” don’t fall into that trap!

The person with the higher score not only has a lower monthly payment, but because they also got a higher Cash Out % which gave them an additional $35,000 out.

Having that good credit score makes it possible to keep cash flowing. If you’re serious about investing, your credit score matters.

Should you look for DSCR loans or are local banks going to have what you need?

Whenever we’re talking about rentals, we’re always going to come back to cash flow, and it’s important to find the best cash-flowing loan.

We want to look at the pros and cons of each type of rental loan to help you understand which might be the best option to help your cash flow for a specific deal.

DSCR Rental Loans

DSCR stands for debt-service coverage ratio. You’ll often see these loans come up for anything from a single family home to a larger multi-unit property.

Pros of DSCR

1. Flexibility. While traditional loans find strength in their consistency, investors sometimes find themselves needed a lot more flexibility. That’s where DSCRs come in.

DSCRs are significantly more flexible because lenders and investors can negotiate unique terms that fit a project’s specific needs.

2. Ease! The biggest benefit of DSCR is ease. It doesn’t matter if you’re employed, what your tax return says, or how much income you have flowing. DSCR lenders only care about the rental property and whether it has the potential to produce cash flow.

3. Close in an LLC. Another big thing in the real estate investor world is closing in an LLC. Unlike traditional bank loans, you can both buy and refinance in an LLC, so you’re protected all the way through.

4. Available in all 50 States. No matter where you are, you will be able to find available DSCR rental loans. However, the details might vary.

Each lender offering DSCRs have their own terms, guidelines, etc. This makes it incredibly important to shop around to make sure you find the right fit.

5. Unlimited Number of Properties. You will find so many options in the DSCR world. You can find loans for specific properties or do a blanket loan for $50 million that could cover as many units as you wanted.

Always make sure that the lender and loan are the right fit for you, and remember that there are a ton of options available!

Cons of DSCR

1. Prepayment Penalties. The number one downside of DSCR loans are the prepayment penalties. If you’re looking to get in and out of a property within the first three to five years, there’s a prepayment penalty unless you buy it out.

2. Higher Rates. Rates for DSCRs typically run anywhere from 1%-3% higher than traditional bank loans, depending on credit score, size of loan, etc.

3. Might Disappear or Change Quickly. DSCR loans are prone to change quickly. When shifts happen in the real estate market, they might even disappear for a brief time before showing up again.

While traditional bank loans are more slow-moving, DSCR moves quickly, and sometimes that can become an issue to real estate investors.

4. Can’t Home Hack. DSCR also does not allow you to live in any of the units you’re working on as you could with an owner-occupied traditional loan.

Local Banks for Rental Loans

Another option that fewer people consider is looking at loans from small, local banks. These local banks sometimes offer in-house products that can offer more flexible loans to people investing in their local area.

Pros of Small Bank Loans

1. More Flexibility. Depending on your area, some local banks love real estate investors. If you shop around and find a small bank willing to invest, these loans often offer more flexibility than larger traditional loans.

Because local banks are more likely to understand the area, unique properties that might seem strange to larger lenders might be more seriously considered by locals.

2. Decent Rates. Rates for local banks typically fall between traditional loans and the higher DSCR rates. However, you do keep more flexibility (the appeal of DSCR) for a lower rate.

3. No Prepay Penalties. Most local banks don’t have the extensive prepay penalties like DSCRs.

4. Good for Smaller Towns and Loans. Banks often want to invest in their local areas, and they’re often more willing to give out smaller loans for those areas as well. Of course, these banks still want to see good income and good credit.

Cons of Local Bank Loans

1. Each is Different. Every small bank makes their own rules. Because of this, its so important to shop around to find a bank that will offer you good rates for your specific project.

2. Lending Limits. Local banks also have lending limits. If you’re putting a portfolio together or doing multiple properties, you might hit up against that lending limit, and the bank might have to step away from offering you a loan.

3. Shop Around. As we already mentioned, one of the big negatives is you have to shop around. Small bank loans can also change like DSCR loans, so just because you talked to a bank at one point doesn’t exclude them from being considered again in the future.

4. Limited Areas/Regions. They also limit their areas and don’t want to go too far out of that market. Look for banks in the local area of your investment property.

5. Callable. Loans from small banks are callable. This means that, if they feel like the values have gone down, they could call the loan and make you pay it off or refinance it somewhere else. Neither traditional nor DSCR loans have this feature.

This gives small bank loans a bit more risk than other types of rental loans.

https://thecashflowcompany.com/wp-content/uploads/2023/07/Screenshot-2023-07-07-120252.png5371033Mike Bhttps://thecashflowcompany.com/wp-content/uploads/2022/09/The-Cash-Flow-Company-logo.pngMike B2023-07-17 08:00:172023-07-20 17:22:28DSCR Loans vs. Local Banks

This loan comparison can help you figure out what loan is right for YOU.

Whenever we’re talking about rentals, we’re always going to come back to cash flow, and it’s important to find the best cash-flowing loan.

We want to look at the pros and cons of each type of rental loan to help you understand which might be the best option to help your cash flow for a specific deal.

Traditional Rental Loans

Pros of Traditional Loans

1. It’s a 30 Year Mortgage. This standardized timeline is reliable and consistent across most traditional loans.

2. No Prepay Penalty. Without a prepayment penalty, you can get out of the loan whenever you want. This is great if you anticipate a changing market and might want to sell early.

3. Lower Interest Rates. Between DSCR and traditional rental loans, you’re often looking at at least a whole point difference in the interest rates. While a single percentage might seem small, when you’re dealing with hundreds of thousands of dollars, the interest adds up very quickly, and you should consider it during loan comparison.

Interest rates affect everything from your cash flow to your credit score to your debt ratio. Depending on where you’re at financially, lower interest rates can be a huge point in favor of these traditional loans.

4. Home Hacking. With traditional rental loans, you’re actually able to do an owner-occupied loan. This allows you to live in one of the units you’re working on. Especially if you’re working on multiple units, you can move from one to another as needed.

Sometimes these owner-occupied loans have lower down payments and better rates, so they’re often worth looking into.

5. Same Rules Nationwide. Traditional loans are consistent across the country. No matter where you go, the guidelines are the same. This makes them predictable although they often have stricter guidelines than other loan types.

Cons of Traditional Loans

1. Property Limits. With traditional loans, you’re limited to 10 properties or 10 units. So while they do often have the best rates, you’re limited in how many properties they cover.

2. Need Income Proof and Good Credit. Not all loans need proof of income, but traditional loans certainly do. Your rates will also be limited by your credit score.

3. Cannot Close in an LLC. Unlike other loan options, traditional loans require you to close in your personal name because you cannot own the property when you’re going through a purchase or refinance in an LLC.

An LLC typically works to protect individuals from the financial effects of a business. However, because of the limits of traditional loans, you can’t use that protection in this scenario.

4. One Year Seasoning. You’re not allowed to refinance until after a full year has passed. This is especially important to consider if you’re doing a BRRRR and want to tap into some equity with a full refinance or purchase.

DSCR Rental Loans

DSCR stands for debt-service coverage ratio. You’ll often see these loans come up for anything from a single family home to a larger multi-unit property.

Pros of DSCR

1. Flexibility. While traditional loans find strength in their consistency, investors sometimes find themselves needed a lot more flexibility. That’s where DSCRs come in.

DSCRs are significantly more flexible because lenders and investors can negotiate unique terms that fit a project’s specific needs. When doing your loan comparison, consider how much flexibility you’ll need.

2. Ease! The biggest benefit of DSCR is ease. It doesn’t matter if you’re employed, what your tax return says, or how much income you have flowing. DSCR lenders only care about the rental property and whether it has the potential to produce cash flow.

3. Close in an LLC. Another big thing in the real estate investor world is closing in an LLC. Unlike traditional bank loans, you can both buy and refinance in an LLC, so you’re protected all the way through.

4. Available in all 50 States. No matter where you are, you will be able to find available DSCR rental loans. However, the details might vary.

Each lender offering DSCRs have their own terms, guidelines, etc. This makes it incredibly important to shop around to make sure you find the right fit.

5. Unlimited Number of Properties. You will find so many options in the DSCR world. You can find loans for specific properties or do a blanket loan for $50 million that could cover as many units as you wanted.

Always make sure that the lender and loan are the right fit for you, and remember that there are a ton of options available!

Cons of DSCR

1. Prepayment Penalties. The number one downside of DSCR loans are the prepayment penalties. If you’re looking to get in and out of a property within the first three to five years, there’s a prepayment penalty unless you buy it out.

2. Higher Rates. Rates for DSCRs typically run anywhere from 1%-3% higher than traditional bank loans, depending on credit score, size of loan, etc.

3. Might Disappear or Change Quickly. DSCR loans are prone to change quickly. When shifts happen in the real estate market, they might even disappear for a brief time before showing up again.

While traditional bank loans are more slow-moving, DSCR moves quickly, and sometimes that can become an issue to real estate investors.

4. Can’t Home Hack. DSCR also does not allow you to live in any of the units you’re working on as you could with an owner-occupied traditional loan.

What can DSCR loans do now in 2023 that they couldn’t do last year?

DSCR loans have been around for a long time. In 2023, the real estate climate has experienced a few changes, and knowing how they relate to DSCR loans can help you get ahead of the game.

Changing Landscape for DSCR Loans

While DSCR loans used to be for single-family or 1-4 unit properties, in 2023 we’re seeing DSCR loans explode into multi-family, blanket loans for larger portfolios, and multi-units.

With new options available, you need to know what to look for while remembering that all DSCR companies have specific niches. It’s important to find a lender who understands the particulars of your project.

The Power of Shopping Around

While this isn’t new, shopping around is very important in 2023. With a growing number of lenders loosening their requirements, finding a lender that specializes in projects like yours can make a big difference.

If your project is unique or you’re dissatisfied with the rate you’re offered, reach out to mortgage lenders or brokers who have the power to offer something different.

Exploring DSCR Loan Possibilities in 2023

As a reminder, DSCR loan requirements are based exclusively on income from the property in question (not personal or business income or taxes).

This has allowed for some exciting new developments in the DSCR loan market:

Expanded Property Types:

DSCR loans now cover a wider range of properties, including large portfolios of more than $50 million, blanket loans for mixed-use properties, and larger multi-family units.

The range of these options provide greater flexibility when shopping around for DSCR lenders and exploring their requirements.

Flexible Requirements:

It’s now possible to find DSCR loan options for first time investors and investors who don’t own a primary residence.

This opens up DSCR loan opportunities for investors who were previously more limited in their abilities to purchase investment properties.

Rural Properties and Condotels:

If you’re looking to purchase rural properties, condotels, or other vacation rentals by owner (VRBO), you can now find DSCR loans for properties up to 20 acres.

Funding Considerations for DSCR Loans in 2023

Products change constantly, so it’s always a good idea to talk to professionals in your area, particularly when it comes to how DSCR lenders look at funding, financing limits, and credit:

Gift Funding Flexibility: Lenders are trending towards having looser rules around gift money. Previously, it was better to have seasoned money in your account. Now, so long as the money is there for closing and it comes from your account, you’re usually set. That said, if you have any questions about gift funding, talk to your particular lender.

Property Ownership Limits: A few lenders are also lifting their limits on how many properties you can finance. Previously, the majority of companies limited investors to 5-10 properties. Now, it’s fairly easy to find lenders without those restrictions.

Credit Influence: Although DSCR loans don’t look at your income, they still look at credit. The better the credit score, the better the loan to value ratio. Also, the higher the DSCR calculation (rent ÷ income), the better the terms.

Standard Interest Only Options: As always, there are interest only options. Depending on your project and the current market, these aren’t always the most helpful, but they are available.

How to Find Your DSCR Loan in 2023

With the recent shifts in the 2023 DSCR loan market, you should be able to find a loan option that works for you so long as your project has the potential to draw income.

We’re more than happy to help you shop around to find the best rates.

https://thecashflowcompany.com/wp-content/uploads/2023/06/Jun-23-DSCR-2023-Blog-Thumbnail.png6001800Mike Bhttps://thecashflowcompany.com/wp-content/uploads/2022/09/The-Cash-Flow-Company-logo.pngMike B2023-06-16 08:00:002023-06-14 17:35:32Exploring DSCR in 2023: New Opportunities for Real Estate Investors

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.