Fastest route to generational wealth? Buy real estate in 2023.

2023 will be a great time to buy real estate.

When a recession hits, when interest rates are high… that’s where you create generational wealth.

Let’s look at the math and past examples to prove it.

We’ll go through the market mechanics behind buying in 2023. Plus, we’ll review the success our clients had during the last recession (and show how you can do the same).

The Secret Behind Generational Wealth with Real Estate in 2023

Building generational wealth with real estate depends on interest rates. Let’s run through the math of how it all works.

Interest rates and prices work like a seesaw. When interest rates go up, affordability and buying power go down, so prices go down. When interest rates come down, buyers can afford higher payments, so prices re-inflate.

So, where will we be in 2023, and how will prices play out? Interest rates are projected to be 8% – the highest they’ve been in years. Let’s look at an example of this seesaw effect.

Interest Rate vs Price When Buying Real Estate in 2023

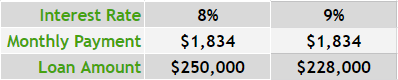

We’ll use 8% as an example, since that’s the projected average for next year. (But this math will work whether your interest rate is 7%, 10%, etc.).

Let’s say our buyer can afford a $250,000 house with an 8% interest rate. We can calculate that their monthly payments would be $1,834.

That monthly payment amount is important. We tend to think of a buyer’s budget as the purchase price they can afford. But really, a buyer’s budget is the monthly payment they can afford.

Even if a buyer is willing to pay a higher purchase price with high interest rates, their lender may stop them. A buyer qualifies for a loan based on the affordability of the monthly payment.

For an interest rate of 8% in 2023, buying power looks like this:

You can plug any numbers you want into this formula to figure out affordability.

For example, let’s say interest rates are 9%. The affordability doesn’t change – our buyer could still only swing a $1,834/month payment. Therefore, this homebuyer’s buying power goes down to $228,000.

Cash Flow with High Interest Rates

As you can see, the higher the interest rate, the lower the price. This is why you should buy while interest rates are high.

Prices will be lower than they have in a while. The challenge is that high interest rates make generating cash flow on properties more difficult. However, even if your rental property only breaks even every month – that’s fine for right now.

A little temporary cash flow loss is worth it when you’re on the path to generational wealth. When interest rates come back down, cash flow will accelerate through the roof.

Let’s flash forward our 2023 example a few years in the future.

Building Equity with Real Estate in 2023

Say we bought that $250k house at 8% in 2023. Three or four years later, the market has stabilized. More money is flowing in the economy and in real estate, driving interest rates back down. Inflation has calmed down to normal levels. Now, let’s say the average interest rate is down to 5%.

What’s the affordability of that 5% rate with our buyer who could qualify for a $1,834/month payment? Now, they can qualify for a $341,000 house.

That means the house you bought for $250k in 2023 could be worth $341k by 2027. This one property could create $91,000 in equity.

Of course, this isn’t a guaranteed timeline or number. But we know it’s close. Real estate operates with the seesaw of rates and prices, affordability and payments.

Refinancing Once Rates Fall

So you have $91,000 in extra equity. But here’s where the cash flow starts to kick in: You can now refinance the property from an 8% rate to 5%.

Your original loan will be down to about $245,000 after 4 years of $1,834 monthly payments. Refinancing $245k at the new 5% interest rate makes for monthly payments of $1,315.

This refinance would increase your monthly cash flow by $519.

Multiply that by 12 months in a year. By 10 more properties… And you’re on the track to generational wealth.

Generational Wealth from the Last Recession

The true “secret” to generational wealth is buying at the right time, then… letting the market take care of itself.

Let’s map out the possibilities if you buy properties while interest is high and prices low, then wait.

Past Client Success

Back in 2010, we helped two families who were particularly successful buy 10 properties each using the BRRRR method.

After 12 years, each of the properties they purchased in 2010 either tripled or quadrupled in value. The rents tripled.

This worked because they bought smart and played the waiting game. They purchased with high rates and low prices, then refinanced once the rates flipped low and values high.

Your Future Success

Let’s say you buy 10 properties in 2023 while rates are high and prices low. Then you hold until the market flips for you – low rates and high values.

You can capture $90k-$100k in equity when the market flips back. Ten properties would add almost $1 million to your net worth.

When you add an extra $500/month in cash flow through a well-timed refinance, that makes for an extra $6,000 in your pocket per year. Multiplied by 10 properties? $60k/year.

All this – just for buying when no one else is buying. Buying when rates are high, values are low, and letting the market correct itself.

Your Plan to Buy Real Estate in 2023

Buying low with high interest rates, waiting, and pulling in the generational wealth. It’s possible with real estate in 2023.

Want to build a game plan for kickstarting your generational wealth next year? Have a deal now you want us to run the numbers on? Send us an email at Info@TheCashFlowCompany.com.