Getting a DSCR loan can feel a bit different from qualifying for a traditional loan. Instead of looking at your income, lenders focus on the property’s ability to pay for itself. Today we are going to walk through a Step-by-Step Guide to Qualifying for a DSCR Loan. This will help you check if a property qualifies. From understanding property income requirements to using a free DSCR calculator, this guide will walk you through each step to make sure you’re ready to get approved.

What Is a DSCR Loan?

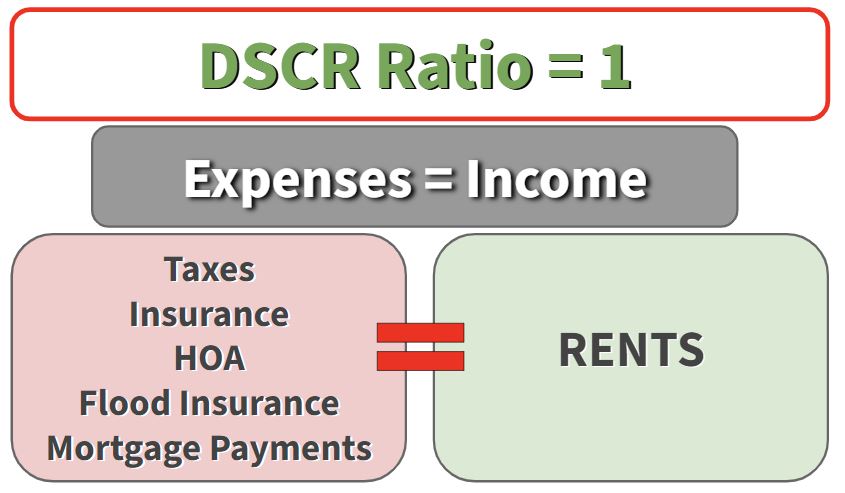

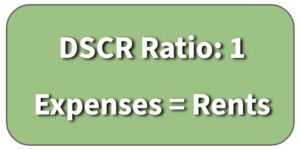

A DSCR (Debt Service Coverage Ratio) loan is a little different from traditional loans. It focuses on the income of the property, not your personal income. In short, it’s all about whether the property can cover its own expenses.

Step 1: Understand the Role of Property Income

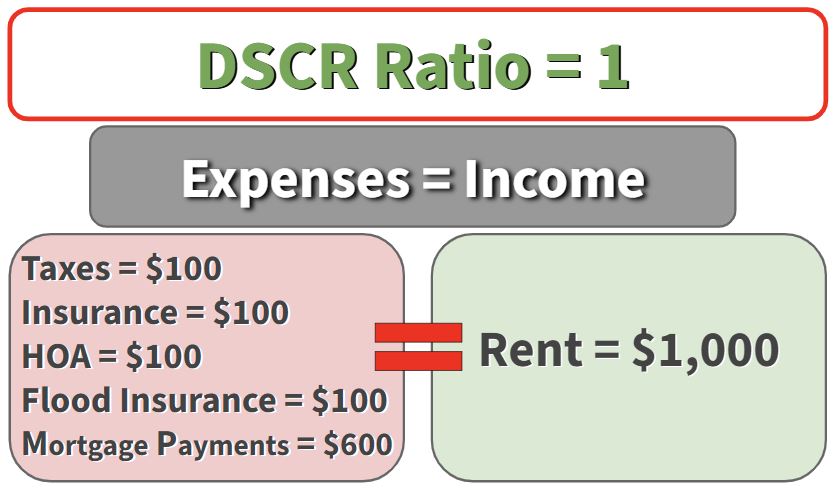

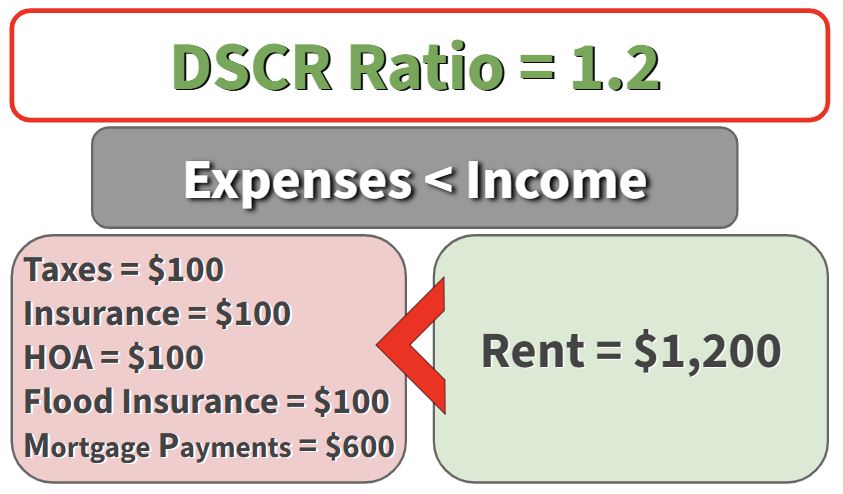

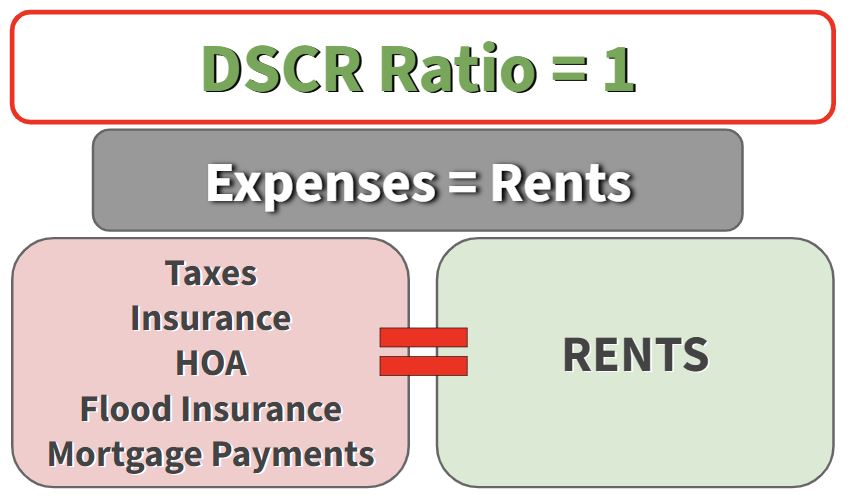

For a DSCR loan, lenders look at the property’s income compared to its expenses. This includes the mortgage payment, property taxes, insurance, HOA fees, and other costs. Here’s the key: if the property’s income can cover these expenses, it may qualify.

For example, let’s say your property earns $1,800 in rent each month. You’ll want to compare this income against the costs. If the income covers these costs, you’re on the right track.

Step 2: Use the DSCR Calculator

The Cash Flow Company offers a free DSCR calculator tool that can help you see if a property qualifies. With this tool, you can run through real scenarios. Let’s walk through an example:

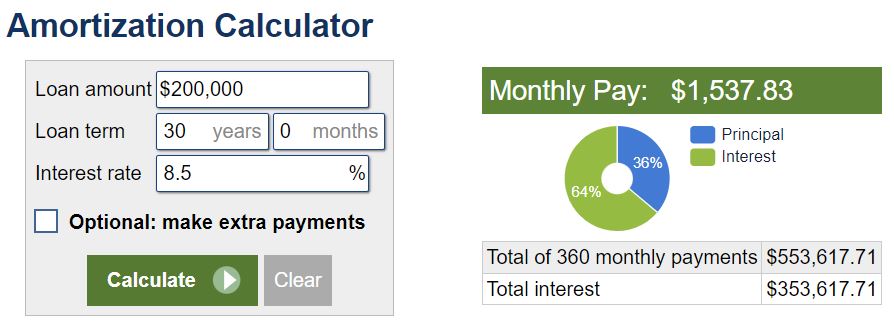

- Property Value: $300,000

- Loan Amount: $240,000 (80% LTV)

- Interest Rate: 6.5%

- Monthly Taxes and Insurance: $450

- Monthly Rent: $1,800

When you plug in these numbers, you’ll see if the property’s DSCR is over 1, which is the qualifying ratio most lenders look for. If not, don’t worry! You can adjust the numbers.

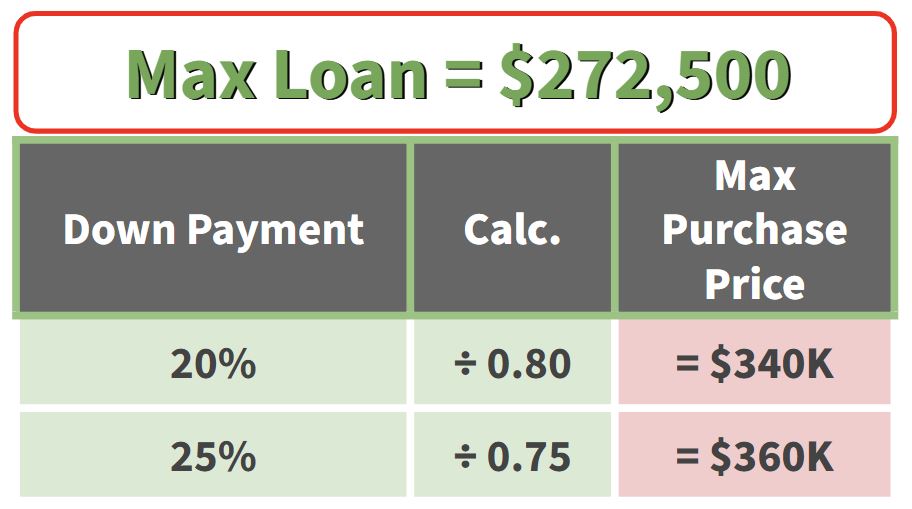

Step 3: Adjust Loan-to-Value (LTV) Ratios if Needed

If your DSCR is below 1, consider adjusting your LTV. In our example, at 80% LTV, the property didn’t qualify because the DSCR was below 1. Dropping to 75% or even 70% might make a difference.

When we lowered the LTV to 75%, the loan amount went down to $225,000. At this point, the DSCR is close to or above 1, showing the property could now qualify.

Step 4: Use Realistic Rent Numbers

Be sure to use accurate rent numbers. An appraiser will check the rent for the neighborhood, so you can’t estimate higher rents than what’s realistic. Use a conservative approach to avoid surprises during the underwriting process.

Step 5: Consider Interest Rates and How They Affect DSCR

Interest rates impact DSCR. If rates go up, your DSCR might drop below 1, meaning the property may not qualify. Some lenders may allow a lower DSCR but at a higher interest rate, which affects profitability.

Final Check: Make Sure It’s a Good Investment

Once you have a DSCR above 1, check if the property will make money or cost you monthly. You want a DSCR loan to boost your investment, not drain it. Use the DSCR calculator tool to run numbers for every property.

Get the Free DSCR Calculator

Head to The Cash Flow Company website and download the free DSCR calculator. This tool is your first step to understanding if a property qualifies before reaching out to lenders.

Need Help?

Knowing whether your property qualifies for a DSCR loan can save you time and effort. Try the DSCR calculator on each potential investment to see if it’s likely to generate positive cash flow. If you have any questions or need guidance on how to use the calculator, reach out to us! With the right prep, you’ll know if your property is set to make you money or if it’s better to pass.

Watch our most recent video to find out more about: A Step-by-Step Guide to Qualifying for a DSCR Loan