How Does Credit Score Impact DSCR Loans?

Categories: Blog Posts

What do you need to know about your DSCR loans so your investing is easy, lucrative, fun, and fast?

DSCRs are investor-friendly loans. Banks calculate these loans based on the break-even point between the income of the property (rents) and the payments for that property (taxes, insurance, HOA, etc.).

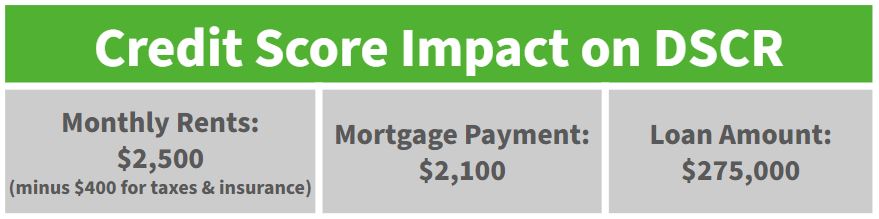

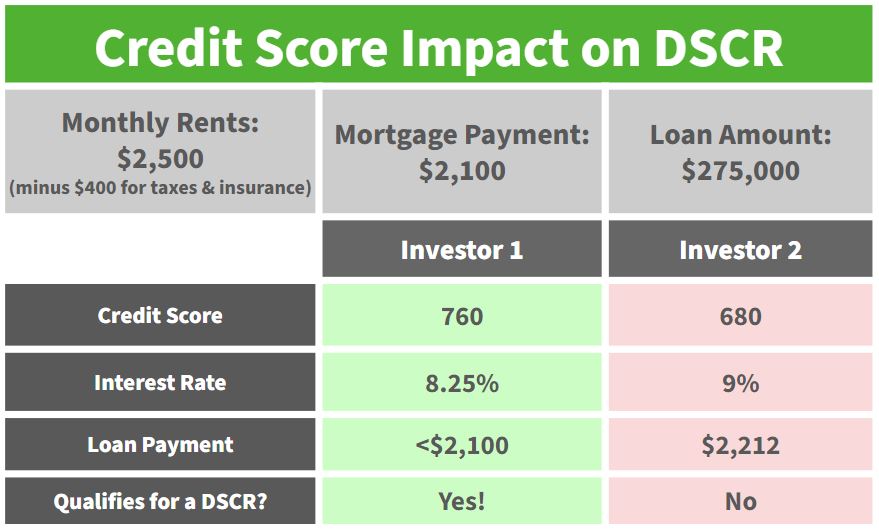

Let’s look at an example to see how credit score can impact your DSCR loans:

Once you subtract your expenses from the monthly rent, you’re left with $2,100. This means that, in order to maintain a DSCR ratio of 1 (the minimum to break even), you need a loan that has monthly payments of $2,100 or lower.

In the following example, Investor 1 has maintained a high credit score while Investor 2 has dipped below most banks’ minimum requirements.

In the two examples above, everything is the same except for the credit scores, and the effect is significant. Investor 2 can’t get a loan to refinance, and they’re either going to have to sell the property or keep their original loan for far longer than they wanted.

Regardless, the person with the higher score is able to move through the investing process easily, lucratively, and quickly.

A bad credit score can tank your leverage and sabotage your investing by creating unnecessary roadblocks for your projects.

In summary, leverage is king, and credit scores are an important piece of your leverage.

A good credit score makes it easier for you to qualify for and refinance your DSCRs. They can also help you put less money down on a property and increase your cash flow.

Take care of your money buckets and credit score on the front end so you can succeed when deals come your way.

Read the full article here.

Watch the full video here: